Airlaid nonwovens are on an attractive growth trajectory, according to the latest exclusive data from Smithers – the leading consultancy for the paper, packaging, and nonwovens industries.

Its report the Future of Airlaid Nonwovens to 2027 shows the market will top $2 billion in sales for the first time in 2022. Further increases are then forecast at a compound annual growth rate (CAGR) of 7.7%, pushing overall market value to $2.93 billion in 2027, at constant prices. Across the same period consumption of airlaid nonwovens products will increase from 574,800 tons to 768,800 tons, equivalent to a CAGR of 6% for 2022-2027.

Sustainable Potential

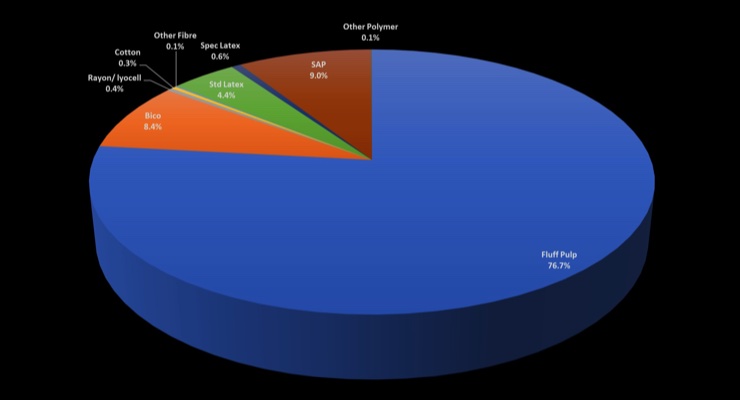

Sustainability is one of the main factors driving the wider use of airlaid nonwovens. With a raw material base that is around three quarters fluff pulp, which is cultivated from softwood trees, is biodegradable and one of the lowest cost raw materials used in nonwovens. Like any industrial process, airlaid production does require energy – primarily natural gas – but it is one of the least energy-intensive nonwoven production technologies and uses little water and few chemicals.

Airlaid market shares by raw materials 2022

Consequently, airlaid provides a strong solution for brands looking to reduce their impact on the environment – including the legislative pressure for more flushable wipe substrates. Innovation is further reducing polymer use. Notably Glatfelter has developed non-plastic binders, which are now being used in some of its airlaid goods.

Sustainability is especially attractive in some major end-use segments, especially feminine hygiene goods (35.8% of the market in 2022, by weight), wipes (23.6%), tabletop media (13.6%), and food pads (9.2%). These are all consumer applications and single-use. In durable and industrial nonwovens, airlaid enjoys a much smaller share with limited used sub-segments, such as cabin air filters in filtration, flame-retardant mattress barrier fabrics, garments and liquid filtration.

Heavier Substrates

Many of the highest volume airlaid segments are heavily consolidated. A few companies dominate supply of traditional airlaid substrates, these vary in weight from 40-300gsm, with the average in the 70-80gsm range. Following its acquisition of Georgia Pacific’s airlaid business and Jacob Holm in 2021, Glatfelter now controls around 30% of now global airlaid capacity – more than the next five producers combined. A further restraint is that airlaid has a steep technological barrier to entry—Fiberweb Italy, Danish Airlaid Technology and Lacell all failed trying tos establish themselves in this market in the past decade.

There is new potential for heavier airlaid substrates, in the 500-1500gsm range. The principle end-use applications for these are in packaging, insulation, and molded consumer products. The heavier substrate segment is an easier market for new firms to attack as they do not have the same requirements for basis weight and density control. Furthermore they are now economically viable due to a recent process modification – using a very open spike former that optimizes throughput at the expense of fine formation control.

What is today a small segment of the market (6.8% by weight in 2022); these are accelerating in demand. In packaging, airlaid is being embraced for is protective and insulating properties, for example in temperature-controlled delivery formats, where it is a more sustainable alternative to existing plastic materials. The same qualities are helping these new airlaid substrates penetrate the home insulation market in place of expanded polystyrene or other foamed plastics.

Molded consumer products are another new market driven by the desire to replace single-use plastics, in formats such as food trays, cutlery and cup lids.

Capacity

The other major challenge for the airlaid segment over the next five years is adding suitable capacity to handle the emergent demand. Airlaid is the smallest of the major nonwovens markets in 2022, and has the tightest demand-capacity ratio, estimated at 92%. Thirty-four major airlaid producers and 24 minor airlaid producers, with 90 commercial lines and a nominal capacity of 624,800 tons of product define the airlaid industry in 2022.

For conventional substrates, new capacity is being added with EAM/Domtar’s starting up a new multibond airlaid manufacturing line in 2022, but no other major expansions have been announced. New capacity will further have to be balanced against the closure of older, less efficient airlaid lines.

This is attributable to a conservative mindset, and a collective memory of the impact of massive capacity increases (+37% in one year) during the early 2000s, a subsequent price collapse, and a round of bankruptcies. For the next five years, this means investment in new airlaid lines will continue to follow below the rate of expansion. Smithers forecasts this will see the demand-capacity ratio increase further to 94% in 2027. In contrast, for the newer heavy substrate markets expansion is happening more quickly, with dedicated lines in commercial production for each of the emergent end-use applications.

Smithers analysis tracks demand across the four leading airlaid processes – multibonded airlaid (MBAL); latex bonded airlaid (LBAL), thermal bonded airlaid (TBAL), and hydrogen bonded airlaid (HBAL).

MBAL is the most flexible of the airlaid processes. It can be used to produce LBAL or TBAL; and in some cases HBAL constructions too. Capable of addressing all traditional airlaid markets, as well as testing some newer markets and end uses; in 2022, TBAL accounts for just over half of global consumption, by weight. MBAL is also the most technically complex process and has the highest capital costs, however.

The fastest growth will come from TBAL, with demand in 2027 forecast to be more than double that in 2021. TBAL lines are cheaper to operate and offer superior emboss quality on the finished product; and is the technology best positioned to benefit from demand for new heavier substrates for applications like green insulation and molded consumer goods.

Detailed expert forecasting for this sector is now available in The Future of Airlaid Nonwovens to 2027, [https://www.smithers.com/en-gb/services/market-reports/nonwovens/the-future-of-airlaid-nonwovens-to-2027] from Smithers. This is founded on an exclusive market dataset segmented by airlaid process, raw material input, end-use application, and geographic region. The current and future market outlook is further contextualized by a detailed examination of emergent market, regulatory, and technology developments; and profiles of the leading eleven global manufacturers. This expert industry study is available to purchase now for $6,750 (€5,970, £5,250). n