David J. Price, Partner, Price Hanna Consultants LLC03.02.18

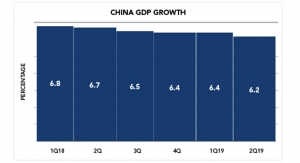

Nonwoven capacity and production demand (in-region demand and exports) in Southeast Asia is expected to continue to grow during 2017–2022 spurred on by favorable economic conditions, local and export market demand and increasing market penetration. Taken as a whole, the ASEAN five countries (Malaysia, Indonesia, Philippines, Thailand and Vietnam) are estimated to be the third largest global market and among the largest global economies. Real GDP growth among the ASEAN five was estimated to have grown at an annual rate of just over 5% in 2017. Real GDP growth in Vietnam and the Philippines grew near or above 7% annually in the final quarters of 2017, higher than in China and other global regions. Real GDP growth in the Philippines from 2018–2022 is expected to remain solid at an average of 7-8%. Attractive Real GDP growth amongst the ASEAN five countries is indicative of rising employment, higher productivity and wages. This, along with good economic conditions in China, Asia Pacific, Southern Asia and other export markets should be favorable for sustained economic conditions in Southeast Asia.

Increasing market penetration for disposable and durable nonwovens in Southeast Asia and China, where market penetration is still low, is a positive predictive factor for good nonwoven demand growth in both Southeast Asian markets and in their export markets as well. Nonwoven producers in the ASEAN five countries are expected to benefit from good export demand from China, Japan and other countries in and outside the Asia Pacific region. The largest market for converted nonwoven products will be in hygiene end uses followed by nonwovens used in durable geotextile and other markets.

In 2018, nonwovens capacity in the region consists largely of spunbonded/spunmelt fine denier technology followed by carded staple fiber needlepunched and/or thermal bonded capacity, spunbonded polyester and medium denier spunbonded polypropylene needlepunched technology. Small but growing installations of other nonwoven technologies including carded air through bonded are also present.

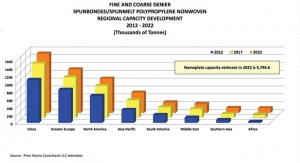

From 2012-2017, the installation of fine denier spunbonded and spunmelt polypropylene nameplate capacity in Southeast Asia grew an average of 13% annually from 139,000 tons to 256,000 tons. Nameplate capacity of this technology increased to 276,000 tons in 2018.

In 2018, the nameplate capacity of both fine and medium denier spunbonded/spunmelt polypropylene technology in the Southeast Asia is 285,000 tons and accounts for about 7% of all global capacity in this technology category.

The largest concentration of this capacity is in Thailand where 47% or 134,000 tons of all spunbonded nonwoven capacity is now present among four different producers. In Malaysia, there are now two producers who have a total capacity of 94,000 tons of this capacity in place which accounts for 33% of the total capacity in Southeast Asia. In Indonesia, there are now two producers who have 52,000 tons of this capacity in operation which is equal to 18% of all capacity in the region. The remaining capacity of this technology in the region is in the Philippines.

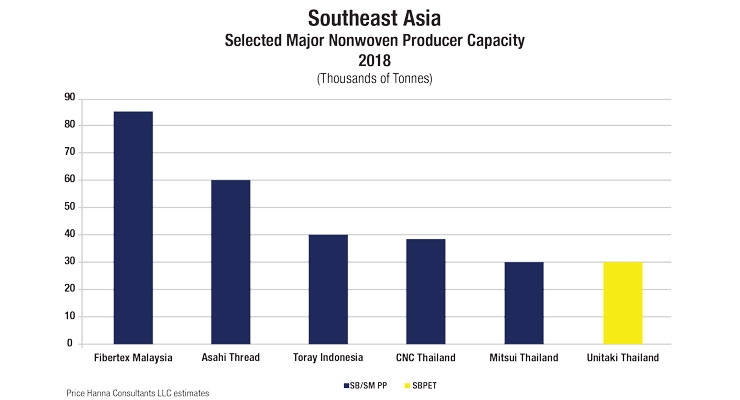

Most of the largest producers of nonwovens in Southeast Asia utilize fine denier polypropylene spunbonded/spunmelt technology only and largely supply the hygiene market. Fibertex in Malaysia is the largest nonwoven producer in Southeast Asia in 2018 with capacity of 88,000 tons.

Asahi (Thailand) will commission a new line in 2018 and will have 60,000 tons of fine denier spunbonded capacity by year end. CNC and Mitsui, both in Thailand, will have about 40,000 tons and 30,000 tons, respectively, of fine denier capacity in 2018.

Unitika commissioned a 30,000 ton spunbonded polyester line in 2017 making them the sixth largest nonwoven producer in Southeast Asia. Nonwovens from this line will be used in carpet backing, geotextiles, roofing, automotive and other industrial applications.

Ten Cate is the only producer of medium denier spunbonded polypropylene nonwovens in Southeast Asia. These nonwovens are needlepunched and supply the geotextile market and other related end uses. Ten Cate’s annual nameplate capacity is 9000 tons and is unchanged since 1996.

Spunbonded/spunmelt fine denier producers in Southeast Asia will remain heavily dependent upon exports to achieve acceptable levels of capacity utilization. Disposable nonwoven demand is growing but remains quite small compared to installed capacity within the region.

David J. Price is the author of the Price Hanna Consultants LLC annual subscription report “Spunbonded and Spunmelt Nonwoven Polypropylene World Capacities, Supply/Demand, Manufacturing Economics and Profitability.” The most recent report was published in October 2017 covering the period 2012, 2017 - 2022. To obtain a detailed prospectus for this study, please contact Michele Scannapieco, Price Hanna Consultants LLC, at mscannapieco@pricehanna.com.

Increasing market penetration for disposable and durable nonwovens in Southeast Asia and China, where market penetration is still low, is a positive predictive factor for good nonwoven demand growth in both Southeast Asian markets and in their export markets as well. Nonwoven producers in the ASEAN five countries are expected to benefit from good export demand from China, Japan and other countries in and outside the Asia Pacific region. The largest market for converted nonwoven products will be in hygiene end uses followed by nonwovens used in durable geotextile and other markets.

In 2018, nonwovens capacity in the region consists largely of spunbonded/spunmelt fine denier technology followed by carded staple fiber needlepunched and/or thermal bonded capacity, spunbonded polyester and medium denier spunbonded polypropylene needlepunched technology. Small but growing installations of other nonwoven technologies including carded air through bonded are also present.

From 2012-2017, the installation of fine denier spunbonded and spunmelt polypropylene nameplate capacity in Southeast Asia grew an average of 13% annually from 139,000 tons to 256,000 tons. Nameplate capacity of this technology increased to 276,000 tons in 2018.

In 2018, the nameplate capacity of both fine and medium denier spunbonded/spunmelt polypropylene technology in the Southeast Asia is 285,000 tons and accounts for about 7% of all global capacity in this technology category.

The largest concentration of this capacity is in Thailand where 47% or 134,000 tons of all spunbonded nonwoven capacity is now present among four different producers. In Malaysia, there are now two producers who have a total capacity of 94,000 tons of this capacity in place which accounts for 33% of the total capacity in Southeast Asia. In Indonesia, there are now two producers who have 52,000 tons of this capacity in operation which is equal to 18% of all capacity in the region. The remaining capacity of this technology in the region is in the Philippines.

Most of the largest producers of nonwovens in Southeast Asia utilize fine denier polypropylene spunbonded/spunmelt technology only and largely supply the hygiene market. Fibertex in Malaysia is the largest nonwoven producer in Southeast Asia in 2018 with capacity of 88,000 tons.

Asahi (Thailand) will commission a new line in 2018 and will have 60,000 tons of fine denier spunbonded capacity by year end. CNC and Mitsui, both in Thailand, will have about 40,000 tons and 30,000 tons, respectively, of fine denier capacity in 2018.

Unitika commissioned a 30,000 ton spunbonded polyester line in 2017 making them the sixth largest nonwoven producer in Southeast Asia. Nonwovens from this line will be used in carpet backing, geotextiles, roofing, automotive and other industrial applications.

Ten Cate is the only producer of medium denier spunbonded polypropylene nonwovens in Southeast Asia. These nonwovens are needlepunched and supply the geotextile market and other related end uses. Ten Cate’s annual nameplate capacity is 9000 tons and is unchanged since 1996.

Spunbonded/spunmelt fine denier producers in Southeast Asia will remain heavily dependent upon exports to achieve acceptable levels of capacity utilization. Disposable nonwoven demand is growing but remains quite small compared to installed capacity within the region.

David J. Price is the author of the Price Hanna Consultants LLC annual subscription report “Spunbonded and Spunmelt Nonwoven Polypropylene World Capacities, Supply/Demand, Manufacturing Economics and Profitability.” The most recent report was published in October 2017 covering the period 2012, 2017 - 2022. To obtain a detailed prospectus for this study, please contact Michele Scannapieco, Price Hanna Consultants LLC, at mscannapieco@pricehanna.com.