Karen McIntyre, editor12.03.14

The year 2014 included investments, mergers and acquisitions and government regulations that will surely impact the nonwovens industry for years to come. While growth is continuing in nonwovens, it seems to be coming from different sources as investments in new regions and new technologies dominate the headlines. Additionally, the marriage of some of the world’s largest nonwovens producers has created new powerhouses in the industry that will guide developments moving forward.

While many new stories were important to the global nonwovens industry, the following headlines stood out as having the most lasting impact on the shape of the future of nonwovens.

The EPA Wiper Rule

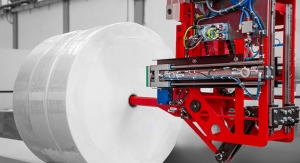

Last year, the industrial wiper market got the good news it had been waiting for. After 30 years of back and forth, the U.S. Environmental Protection Agency (EPA) finally published its long-awaited wiper rule, helping to level the regulatory playing field between non-laundered wipes and rags and laundered shop towels. In 2014, more states adopted the ruling and wipes makers starting ramping up new product development to meet the needs of this market.

The industrial wipes market is expected to grow following the EPA wiper ruling.

The final rule modifies the hazardous waste management regulations under the Resource Conservation and Recovery Act (RCRA) to conditionally exclude solvent-contaminated wipes from hazardous waste regulations provided that the businesses clean or dispose of them properly. It’s based on the EPA’s final risk analysis that concluded wipes contaminated with certain hazardous solvents do no pose significant risk to human health and the environment when managed properly.

To be excluded, solvent-contaminated wipes must be managed in closed labeled containers and cannot contain free liquids when sent for cleaning or disposal, the EPA says. Additionally, facilities that generate solvent-contaminated wipes must comply with certain record keeping requirements and may not accumulate wipes for longer than 180 days.

The EPA estimates that the final rule will result in net savings of $18 million per year in avoided regulatory costs and between $3.7 and $9.9 million per year in other expected benefits, including pollution prevention, waste minimization and fire prevention. Now that the ruling, which was first challenged in the early 1980s, has been finalized, wipes makers are waiting for individual states to adopt the ruling. So far, at least 12 states have already adopted the ruling, while only five have decided against adopting the ruling. Another 25 states have indicated they are very likely to implement the ruling. As this ruling slowly becomes law, INDA, the Association of the Nonwovens Fabrics industry, has formed a Product Stewardship Committee on industrial wipes, a committee to specifically focus on helping wipes companies fully realize the benefits of the wiper rule. INDA is tracking state adoption and weighing-in with officials but will use the new committee to give association members the information and tools to monitor and influence activity in states critical to their businesses and to communicate key details to customers.

Calling the ruling a driver of change in the nonwovens industry, INDA says there is significant marketing opportunity for non-laundered wipes. If nonwoven disposables were to capture 25% over the next three years of the market, the industry would see an annual growth rate increase from 6.1% to 13.3%. Raising the overall industrial and institutional wipes annual growth rate from 5.9% to 8.4%. This represents a significant opportunity.

According to INDA figures, in 2012, sales to end users in the industrial and institutional wipes market were almost $2.8 billion for disposable nonwoven wipes, disposable cloth towels/rags and reusable laundered shop towels/wipes. Sixty percent of these sales were to one segment, the industrial general purpose segment, where the greatest opportunity exists for nonwovens following the Wiper Rule.

Executives doing business in the industrial wipes market agree that there is significant opportunity for nonwovens in this market as more states adopt the ruling. Not only does conversion of nonwovens have the potential to save manufacturers money, the use of these substrates—which can be engineered for task-specific purposes—can get the job done more quickly and completely with less effort.

“Nonwovens offer many advantages in the wiping category. They can be engineered to work with the range of chemistries used in the industrial wipes segment,” says Trevor Kelley, Tork wiper product manager for SCA’s AFH Professional Hygiene business. “This allows you to really get optimal performance.”

The conversion from reusable textile wipers to nonwoven ones would be a paradigm shift in the market similar to the one the diaper market underwent when disposables were first developed in the 1960s.

“A lot of people will be hesitant to make the change. They feel like this is what we have always done and we will stick to it,” Kelley says. “It always takes some time for a market to make the transition to a disposable environment and when users of textiles first look at disposables, they think there is no way a nonwoven can measure up. The best way to encourage the shift is to prove them wrong through trial.”

Flushability

Ever since the third edition of INDA/EDANA’s flushability guidelines were introduced in late 2013, the entire wipes industry has been focusing strongly on getting products that have passed the standards to market. Nonwovens trade associations INDA and EDANA first began working on the guidelines in 2004 with a special taskforce featuring representatives from 31 companies. The first set of guidelines were published in 2008 and a second in 2009. The third set, launched at the end of last year, were designed to simplify the guidelines and make them more user friendly.

Wipes leader Suominen has been one company that has aggressively invested in flushable technology. Its Hydraspun material is made of wood pulp, Tencel and bicomponent fibers and is currently used by Rockline and Procter & Gamble in North America and Kimberly-Clark in Europe. Suominen is investing to add capacity of the material, which has been certified flushable under the standards, in the U.S. and Europe.

Meanwhile, on the machinery front, Fleissner and Voith Paper have teamed up to develop machinery that has created nonwoven substrates that pass the standards, while flushable substrates made by Andritz Perfojet have been available for some time.

Moist tissue is the largest segment of the flushable wipes segment and comprises wet toilet paper products like Cottonelle, Charmin Freshmates and Scott moist wipes as well as a number of store brand products. Other market segments include kids wipes, like Kandoo, feminine hygiene wipes, adult incontinence wipes and bath wipes. According to INDA, the size of the North American toilet tissue and toddler training wipes market is about 21,400 tons, growing between 6-6.5% per year.

PGI continues to grow

During the past 18 months or so, Polymer Group, Inc., has been on an aggressive drive to become the world’s largest nonwovens producer, and in 2014, the company got closer to this goal through the acquisition of Companhia Providencia and the announcement of major investments in both the U.S. and Europe.

“At PGI, we believe that the industry can benefit from a strong industry player,” says CEO J. Joel Hackney. In addition to Companhia Providencia, the company acquired major nonwovens producer Fiberweb in late 2013. Together the two companies add about $700,000 in sales to PGI’s revenues and open it up to new geographies (Providencia) and technologies (Fiberweb). “Fiberweb diversifies PGI from a portfolio perspective, adds some significant research and development activities as well as some tremendous talent,” Hackney continues.

Included in the Fiberweb deal were a large industrial nonwovens and geosynthetics businesses with operations in North America and Europe; Companhia Providencia was a leading producer of spunmelt nonwovens for hygiene and medical applications with state-of-the-art assets in Brazil and South Carolina.

In addition to increasing sales, the acquisitions have broadened PGI’s product range which now includes S-Tex, bicomponent materials made by Providencia and Premium Soft, a technology made by PGI in the U.S. and in China.

In fact, PGI announced several additions to its “soft” line of products in September, which address the need of the baby care, incontinence and feminine hygiene market offerings solutions for visual, tactile and haptic soft properties.

PGI has also been focusing on capital investment to propel growth. In September, the company said it would increase its European output with investments in Spain and Italy. These two investments—spunmelt capacity in Spain and a carded line in Italy—should bring PGI’s total regional capacity to above 100,000 metric tons when they are complete sometime next year.

“PGI is constantly evolving its technologies to help our customers grow,” comments Jean-Marc Galvez, PGI president, Europe. “This capacity increases PGI’s position to assist customers with growing demand for specialty materials in hygiene and healthcare applications.”

Currently, about 27% of PGI’s revenues are generated in Europe, where the company operates four manufacturing facilities in France, Holland, Italy and Spain. PGI acquired the Spanish facility from Telsaca-Texnovo in 2009. At the time of the acquisition the site was capable of making 50,000 metric tons of nonwovens on six lines and reported sales of about $87 million.

Meanwhile, PGI has also expanded its Spinlace technology, for the wipes market, with the construction of a second line in North Carolina, and other recent investments have included investments in Virginia and China.

Jacob Holm buys Sontara

One of the year’s most surprising acquisitions was Jacob Holm’s purchase of Sontara spunlace technology from DuPont, over the summer. The acquisition not only broadens Jacob Holm’s presence in the spunlace market and significantly expands its sales, it also provides it with exposure to some important new markets for spunlace.

“It was a good opportunity for Jacob Holm to create a new industry innovation leader for spunlace by combining the two businesses,” said Jacob Holm CEO Martin Mikkelsen at the time of the acquisition. “It also shows significant growth for us.”

Adding that the acquisition also gives Jacob Holm a broader range of technological nuances within spunlace, Mikkelsen says that Sontara differs from his company’s existing technologies in terms of carding technology and pulp inclusion. Sontara has found success in a number of niche wipes markets, like cleanroom and printing, as well as in a number of medical applications, areas that lie outside of Jacob Holm’s core markets of hygiene and wet wipes.

While spunlaced nonwovens have been challenged by improved grades of spunbond and spunmelt fabrics in recent years, Mikkelsen says there continues to be a preference for spunlace in certain areas of the medical market.

“There are critical areas where spunlace is preferred,” he says. “We have validated that Sontara continues to have a strong position in the medical market and with the right development efforts we will be able to unlock some of the growth potential for spunlace in medical.”

DuPont developed Sontara more than 40 years ago and it is currently made at sites in Old Hickory, TN and Asturias, Spain, which will continue to be operated by Jacob Holm. According to DuPont’s annual report, Sontara sales last year were about $190 million, or 5% of DuPont Protection Technologies’ sales.

Acquisitions

While the acquisition of Sontara by Jacob Holm and Providencia by PGI were certainly big news stories this year, they were not the only major acquisitions on the books in 2014. In fact, 2013-2014 has been a period ripe with acquisition, where we have seen considerable consolidation among the top players in nonwovens.

Among the leading players in nonwovens, Andrew Industries, a maker of baghouse filtration products, is the latest company to disappear. The company was bought out by Lydall in 2014. According to executives, the deal adds about $120 million to Lydall’s sales and creates a new division at the company—Industrial Filtration. This new division complements Lydall’s Performance Materials division, which makes wetlaid nonwovens for filtration and insulations materials. The deal also includes Andrew’s production facilities in the U.S., the U.K. and China.

“The acquisition of Andrew Filtration expands our global footprint, adds complementary and new technologies as well as substantial scale that provides a platform for long-term growth and better positions us to deliver meaningful shareholder value,” said CEO Dale Barnhart at the time of the acquisition. “Lydall’s filtration and engineered materials segments are expected to contribute approximately 50% of Lydall’s consolidated revenue. We expect new growth opportunities will result from manufacturing and selling complementary products and leveraging Andrew Filtration’s well established presence in faster growing Asian markets.”

In October, Danish nonwovens producer Fibertex Nonwovens, a leader in the European industrial nonwovens market, gained access to the U.S. market through the acquisition of Non Woven Solutions (NWS), a Chicago, IL-based manufacturer of needlepunch nonwovens with 2013 sales of nearly $17 million. The deal was valued at $25 million.

According to Fibertex executives, the acquisition was a logical next step for the strategic development of the company, which, in recent years, has expanded through acquisition in France and the Czech Republic and the creation of a greenfield site in South Africa.

“In recent years, Fibertex Nonwovens has increasingly focused on special-purpose products for the composites, automotive and other industries. NWS is a perfect match for this strategy,” says Jørgen Bech Madsen, CEO, Fibertex Nonwovens.

NWS was founded in 2007 and has generated double-digit growth rates in recent years. The company operates two production lines, manufacturing materials for the composites and automotive industries as well as nonwoven products for wound care, filtration, bedding and construction.

Meanwhile, Fibertex Nonwovens’s sister company Fibertex Personal Care purchased a 100% stake in Innowo Print, a company that specializes in printing on nonwovens. Fibertex helped found this company several years ago and maintained a partial ownership stake until recently.

“At Fibertex Personal Care, we mostly manufacture standardized products in very large volumes,” says CEO Mikael Staal Axelsen. “That makes it important for us to offer a uniformly high quality and provide excellent service to our customers. Direct printing on nonwovens is a field where we can differentiate from our competitors in the rest of the market and provide a service that complements our core product. For this reason, acquiring Innowo Print is an important strategic move for us.”

Expansion continues

The investments keep coming in nonwovens. While the pace of new lines has slowed, new lines, across multiple technologies, continue to be announced around the world. In Eastern Europe and Russia, Union Industries and Avgol Nonwovens, are building lines in Poland and Russia, respectively. Both based on spunmelt technology, these lines will serve demand for hygiene products in Eastern and Western Europe.

Moving westward, PGI’s new lines in Spain and Italy are not the only new ones planned for Western Europe. Fitesa recently confirmed it was constructing a new spunmelt line in Sweden, one of many new lines planned by Fitesa. The Brazilian nonwovens producer, who became a market leader two years ago when it purchased Fiberweb’s hygiene-related assets, has also announced plans to add capacity to an existing operation in Lima, Peru and construct a 20,000-ton line at a new site in Sao Paulo, Brazil, and completed work on a second line, capable of making 20,000 tons of material, in South Carolina and a carded line in Tianjin, China.

Meanwhile, in the U.S., spunmelt investment has slowed as Companhia Providencia/PGI’s new line in Statesville, NC recently came onstream but investments have been made in other technologies These include a nano/filtration line from PGI in Waynesboro, VA; spunlace lines from Spuntech and Jacob Holm in North Carolina and an electrostatically charged filtration line from Hollingsworth & Vose in Virginia, to name a few.

P&G is back in incontinence

In August, Procter & Gamble ended months of industry speculation by announcing its return to the adult incontinence market through the launch of Always Discreet, a line designed to change the way women manage their sensitive bladders.

A leader in other hygiene markets like baby diapers and feminine hygiene, P&G had previously been involved in adult incontinence until it sold its Attends business in 1998. Industry insiders had predicted P&G’s return to adult incontinence, a market that offers significantly more growth potential than similar absorbent markets.

The new line consists of liners, pads and underwear designed to offer comfort, protection and discretion, in a feminine design, that absorbs leaks and odors quickly. According to P&G, Always Discreet pads are up to 40% thinner than the leading brand and absorb twice as much fluid as women may need, based on the average consumer usage of incontinence products. The curve-hugging, disposable Always Discreet underwear is designed to be easy to wear and discreet, with the extra protection of Dual LeakGuard barriers to help stop leaks where they are most likely to occur.

P&G is building off the success of its Always feminine hygiene brand, which has provided protection for more than 30 years. With Always Discreet, the brand continues to support women in all phases of their lives with the comfort and protection they’ve come to expect from Always. According to sources familiar with incontinence trends, about 40% of current Always feminine hygiene customers use the products to handle incontinence problems.

“Always Discreet products have undergone extensive consumer testing and are specifically designed to provide the things that matter most to women with sensitive bladders, including odor neutralization protection and discretion,’’ said Chandrika Kasturi, Always Discreet product research director. “Our advanced OdorLock technology traps odors instantly and for hours and our innovative Advanced Core Technology absorbs fluids to the core and locks it away, offering incredible dryness protection.”

P&G began test marketing Always Discreet liners in the U.K. a few months ago and the hygiene industry has been speculating that a North American launch was imminent. The company exited the adult incontinence market, which it helped create in the 1970s, in 1999 when it sold its Attends brand to PaperPak Industries.

Adult incontinence growth

The news that P&G would reenter adult incontinence came as no surprise because of the high level of growth being seen in adult incontinence. During the last 15 years, roughly the amount of time P&G had been absent from the market—North American adult incontinence sales have tripled to reach $1.5 billion, according to experts. Global sales, now at $7 billion, are growing about 8.4% annually, faster than any other paper-based household products.

With an estimated 25 million Americans experiencing incontinence symptoms, manufacturers are coming up with more solutions to these products.

Traditionally, the market leader has been Kimberly-Clark with its Depend and Poise brands, and this company has been launching a steady stream of incontinence items including X.

Meanwhile, industry newcomer Butterfly brands has received laurels for its body liners, which meets the needs of sufferers of accidental bowel leakage (ABL). Last year at Vision, the company received an award for the product, which is being called a category creating innovation and is already meeting the needs of many ADL sufferers, a condition that affects about 20% of women over the age of 40.

While Butterfly brands and P&G are newcomers to adult incontinence, market veteran Kimberly-Clark has made numerous efforts to make sure this business meets the needs of as many people as possible. Recent product introductions or innovations have included male guards and better fitting adult diapers.

These efforts will surely pay off in the long, if not near, term. Already, there are signs that the adult incontinence market could challenge the disposable baby diaper market in terms of sales and volumes. Reports coming out of Japan indicate that adult diapers are outselling baby diapers, where nearly one in every four people is over 65 years old.

While the U.S. market is not quite as dominated by adult incontinence, INDA estimated that adult incontinence product sales will outpace boy baby diapers and feminine hygiene products with an annual growth rate of 3.5%.

Growth continues for nonwovens

Global demand for nonwovens is forecast to rise 5.3% annually to nine metric tons in 2017. However, there is a great deal of variation among different regions and countries, according to market research. Countries with well developed manufacturing sectors and a population with relatively high personal incomes, such as the U.S., Japan, and West European countries, have well established nonwovens markets. In these areas, nonwovens are prevalent in the production of a variety of goods, and individuals have the financial capability to purchase nonwoven-based consumer items.

Most experts agree that demand for nonwovens in developed countries is expected to accelerate from the pace set from 2007-2012, when recessionary conditions for most of the period brought outright declines in manufacturing and construction activity. Despite the acceleration, growth in nonwovens demand in developed areas will remain well below the global average as continued industrialization and increasing personal incomes in developing countries promote nonwovens demand.

Ongoing economic advances in China and other developing countries will promote the development of manufacturing sectors, providing opportunities for nonwovens in a variety of goods, such as filters. With respect to consumer goods, rising incomes and standards of living will propel individuals to purchase convenience items, promoting the production of disposable infant diapers among other items that are made with significant amounts of nonwoven fabrics. The largest regional market for nonwovens is the Asia Pacific region, with 39% of the global total. Two of the top three nonwovens consuming countries—China and Japan—are located in the region. Advances will be driven by China, which will account for 60% of the regional sales in 2017 and nearly 40% of additional global volume demand through 2017.

While many new stories were important to the global nonwovens industry, the following headlines stood out as having the most lasting impact on the shape of the future of nonwovens.

The EPA Wiper Rule

Last year, the industrial wiper market got the good news it had been waiting for. After 30 years of back and forth, the U.S. Environmental Protection Agency (EPA) finally published its long-awaited wiper rule, helping to level the regulatory playing field between non-laundered wipes and rags and laundered shop towels. In 2014, more states adopted the ruling and wipes makers starting ramping up new product development to meet the needs of this market.

The industrial wipes market is expected to grow following the EPA wiper ruling.

To be excluded, solvent-contaminated wipes must be managed in closed labeled containers and cannot contain free liquids when sent for cleaning or disposal, the EPA says. Additionally, facilities that generate solvent-contaminated wipes must comply with certain record keeping requirements and may not accumulate wipes for longer than 180 days.

The EPA estimates that the final rule will result in net savings of $18 million per year in avoided regulatory costs and between $3.7 and $9.9 million per year in other expected benefits, including pollution prevention, waste minimization and fire prevention. Now that the ruling, which was first challenged in the early 1980s, has been finalized, wipes makers are waiting for individual states to adopt the ruling. So far, at least 12 states have already adopted the ruling, while only five have decided against adopting the ruling. Another 25 states have indicated they are very likely to implement the ruling. As this ruling slowly becomes law, INDA, the Association of the Nonwovens Fabrics industry, has formed a Product Stewardship Committee on industrial wipes, a committee to specifically focus on helping wipes companies fully realize the benefits of the wiper rule. INDA is tracking state adoption and weighing-in with officials but will use the new committee to give association members the information and tools to monitor and influence activity in states critical to their businesses and to communicate key details to customers.

Calling the ruling a driver of change in the nonwovens industry, INDA says there is significant marketing opportunity for non-laundered wipes. If nonwoven disposables were to capture 25% over the next three years of the market, the industry would see an annual growth rate increase from 6.1% to 13.3%. Raising the overall industrial and institutional wipes annual growth rate from 5.9% to 8.4%. This represents a significant opportunity.

According to INDA figures, in 2012, sales to end users in the industrial and institutional wipes market were almost $2.8 billion for disposable nonwoven wipes, disposable cloth towels/rags and reusable laundered shop towels/wipes. Sixty percent of these sales were to one segment, the industrial general purpose segment, where the greatest opportunity exists for nonwovens following the Wiper Rule.

Executives doing business in the industrial wipes market agree that there is significant opportunity for nonwovens in this market as more states adopt the ruling. Not only does conversion of nonwovens have the potential to save manufacturers money, the use of these substrates—which can be engineered for task-specific purposes—can get the job done more quickly and completely with less effort.

“Nonwovens offer many advantages in the wiping category. They can be engineered to work with the range of chemistries used in the industrial wipes segment,” says Trevor Kelley, Tork wiper product manager for SCA’s AFH Professional Hygiene business. “This allows you to really get optimal performance.”

The conversion from reusable textile wipers to nonwoven ones would be a paradigm shift in the market similar to the one the diaper market underwent when disposables were first developed in the 1960s.

“A lot of people will be hesitant to make the change. They feel like this is what we have always done and we will stick to it,” Kelley says. “It always takes some time for a market to make the transition to a disposable environment and when users of textiles first look at disposables, they think there is no way a nonwoven can measure up. The best way to encourage the shift is to prove them wrong through trial.”

Flushability

Ever since the third edition of INDA/EDANA’s flushability guidelines were introduced in late 2013, the entire wipes industry has been focusing strongly on getting products that have passed the standards to market. Nonwovens trade associations INDA and EDANA first began working on the guidelines in 2004 with a special taskforce featuring representatives from 31 companies. The first set of guidelines were published in 2008 and a second in 2009. The third set, launched at the end of last year, were designed to simplify the guidelines and make them more user friendly.

Wipes leader Suominen has been one company that has aggressively invested in flushable technology. Its Hydraspun material is made of wood pulp, Tencel and bicomponent fibers and is currently used by Rockline and Procter & Gamble in North America and Kimberly-Clark in Europe. Suominen is investing to add capacity of the material, which has been certified flushable under the standards, in the U.S. and Europe.

Meanwhile, on the machinery front, Fleissner and Voith Paper have teamed up to develop machinery that has created nonwoven substrates that pass the standards, while flushable substrates made by Andritz Perfojet have been available for some time.

Moist tissue is the largest segment of the flushable wipes segment and comprises wet toilet paper products like Cottonelle, Charmin Freshmates and Scott moist wipes as well as a number of store brand products. Other market segments include kids wipes, like Kandoo, feminine hygiene wipes, adult incontinence wipes and bath wipes. According to INDA, the size of the North American toilet tissue and toddler training wipes market is about 21,400 tons, growing between 6-6.5% per year.

PGI continues to grow

During the past 18 months or so, Polymer Group, Inc., has been on an aggressive drive to become the world’s largest nonwovens producer, and in 2014, the company got closer to this goal through the acquisition of Companhia Providencia and the announcement of major investments in both the U.S. and Europe.

“At PGI, we believe that the industry can benefit from a strong industry player,” says CEO J. Joel Hackney. In addition to Companhia Providencia, the company acquired major nonwovens producer Fiberweb in late 2013. Together the two companies add about $700,000 in sales to PGI’s revenues and open it up to new geographies (Providencia) and technologies (Fiberweb). “Fiberweb diversifies PGI from a portfolio perspective, adds some significant research and development activities as well as some tremendous talent,” Hackney continues.

Included in the Fiberweb deal were a large industrial nonwovens and geosynthetics businesses with operations in North America and Europe; Companhia Providencia was a leading producer of spunmelt nonwovens for hygiene and medical applications with state-of-the-art assets in Brazil and South Carolina.

In addition to increasing sales, the acquisitions have broadened PGI’s product range which now includes S-Tex, bicomponent materials made by Providencia and Premium Soft, a technology made by PGI in the U.S. and in China.

In fact, PGI announced several additions to its “soft” line of products in September, which address the need of the baby care, incontinence and feminine hygiene market offerings solutions for visual, tactile and haptic soft properties.

PGI has also been focusing on capital investment to propel growth. In September, the company said it would increase its European output with investments in Spain and Italy. These two investments—spunmelt capacity in Spain and a carded line in Italy—should bring PGI’s total regional capacity to above 100,000 metric tons when they are complete sometime next year.

“PGI is constantly evolving its technologies to help our customers grow,” comments Jean-Marc Galvez, PGI president, Europe. “This capacity increases PGI’s position to assist customers with growing demand for specialty materials in hygiene and healthcare applications.”

Currently, about 27% of PGI’s revenues are generated in Europe, where the company operates four manufacturing facilities in France, Holland, Italy and Spain. PGI acquired the Spanish facility from Telsaca-Texnovo in 2009. At the time of the acquisition the site was capable of making 50,000 metric tons of nonwovens on six lines and reported sales of about $87 million.

Meanwhile, PGI has also expanded its Spinlace technology, for the wipes market, with the construction of a second line in North Carolina, and other recent investments have included investments in Virginia and China.

Jacob Holm buys Sontara

One of the year’s most surprising acquisitions was Jacob Holm’s purchase of Sontara spunlace technology from DuPont, over the summer. The acquisition not only broadens Jacob Holm’s presence in the spunlace market and significantly expands its sales, it also provides it with exposure to some important new markets for spunlace.

“It was a good opportunity for Jacob Holm to create a new industry innovation leader for spunlace by combining the two businesses,” said Jacob Holm CEO Martin Mikkelsen at the time of the acquisition. “It also shows significant growth for us.”

Adding that the acquisition also gives Jacob Holm a broader range of technological nuances within spunlace, Mikkelsen says that Sontara differs from his company’s existing technologies in terms of carding technology and pulp inclusion. Sontara has found success in a number of niche wipes markets, like cleanroom and printing, as well as in a number of medical applications, areas that lie outside of Jacob Holm’s core markets of hygiene and wet wipes.

While spunlaced nonwovens have been challenged by improved grades of spunbond and spunmelt fabrics in recent years, Mikkelsen says there continues to be a preference for spunlace in certain areas of the medical market.

“There are critical areas where spunlace is preferred,” he says. “We have validated that Sontara continues to have a strong position in the medical market and with the right development efforts we will be able to unlock some of the growth potential for spunlace in medical.”

DuPont developed Sontara more than 40 years ago and it is currently made at sites in Old Hickory, TN and Asturias, Spain, which will continue to be operated by Jacob Holm. According to DuPont’s annual report, Sontara sales last year were about $190 million, or 5% of DuPont Protection Technologies’ sales.

Acquisitions

While the acquisition of Sontara by Jacob Holm and Providencia by PGI were certainly big news stories this year, they were not the only major acquisitions on the books in 2014. In fact, 2013-2014 has been a period ripe with acquisition, where we have seen considerable consolidation among the top players in nonwovens.

Among the leading players in nonwovens, Andrew Industries, a maker of baghouse filtration products, is the latest company to disappear. The company was bought out by Lydall in 2014. According to executives, the deal adds about $120 million to Lydall’s sales and creates a new division at the company—Industrial Filtration. This new division complements Lydall’s Performance Materials division, which makes wetlaid nonwovens for filtration and insulations materials. The deal also includes Andrew’s production facilities in the U.S., the U.K. and China.

“The acquisition of Andrew Filtration expands our global footprint, adds complementary and new technologies as well as substantial scale that provides a platform for long-term growth and better positions us to deliver meaningful shareholder value,” said CEO Dale Barnhart at the time of the acquisition. “Lydall’s filtration and engineered materials segments are expected to contribute approximately 50% of Lydall’s consolidated revenue. We expect new growth opportunities will result from manufacturing and selling complementary products and leveraging Andrew Filtration’s well established presence in faster growing Asian markets.”

In October, Danish nonwovens producer Fibertex Nonwovens, a leader in the European industrial nonwovens market, gained access to the U.S. market through the acquisition of Non Woven Solutions (NWS), a Chicago, IL-based manufacturer of needlepunch nonwovens with 2013 sales of nearly $17 million. The deal was valued at $25 million.

According to Fibertex executives, the acquisition was a logical next step for the strategic development of the company, which, in recent years, has expanded through acquisition in France and the Czech Republic and the creation of a greenfield site in South Africa.

“In recent years, Fibertex Nonwovens has increasingly focused on special-purpose products for the composites, automotive and other industries. NWS is a perfect match for this strategy,” says Jørgen Bech Madsen, CEO, Fibertex Nonwovens.

NWS was founded in 2007 and has generated double-digit growth rates in recent years. The company operates two production lines, manufacturing materials for the composites and automotive industries as well as nonwoven products for wound care, filtration, bedding and construction.

Meanwhile, Fibertex Nonwovens’s sister company Fibertex Personal Care purchased a 100% stake in Innowo Print, a company that specializes in printing on nonwovens. Fibertex helped found this company several years ago and maintained a partial ownership stake until recently.

“At Fibertex Personal Care, we mostly manufacture standardized products in very large volumes,” says CEO Mikael Staal Axelsen. “That makes it important for us to offer a uniformly high quality and provide excellent service to our customers. Direct printing on nonwovens is a field where we can differentiate from our competitors in the rest of the market and provide a service that complements our core product. For this reason, acquiring Innowo Print is an important strategic move for us.”

Expansion continues

The investments keep coming in nonwovens. While the pace of new lines has slowed, new lines, across multiple technologies, continue to be announced around the world. In Eastern Europe and Russia, Union Industries and Avgol Nonwovens, are building lines in Poland and Russia, respectively. Both based on spunmelt technology, these lines will serve demand for hygiene products in Eastern and Western Europe.

Moving westward, PGI’s new lines in Spain and Italy are not the only new ones planned for Western Europe. Fitesa recently confirmed it was constructing a new spunmelt line in Sweden, one of many new lines planned by Fitesa. The Brazilian nonwovens producer, who became a market leader two years ago when it purchased Fiberweb’s hygiene-related assets, has also announced plans to add capacity to an existing operation in Lima, Peru and construct a 20,000-ton line at a new site in Sao Paulo, Brazil, and completed work on a second line, capable of making 20,000 tons of material, in South Carolina and a carded line in Tianjin, China.

Meanwhile, in the U.S., spunmelt investment has slowed as Companhia Providencia/PGI’s new line in Statesville, NC recently came onstream but investments have been made in other technologies These include a nano/filtration line from PGI in Waynesboro, VA; spunlace lines from Spuntech and Jacob Holm in North Carolina and an electrostatically charged filtration line from Hollingsworth & Vose in Virginia, to name a few.

P&G is back in incontinence

In August, Procter & Gamble ended months of industry speculation by announcing its return to the adult incontinence market through the launch of Always Discreet, a line designed to change the way women manage their sensitive bladders.

A leader in other hygiene markets like baby diapers and feminine hygiene, P&G had previously been involved in adult incontinence until it sold its Attends business in 1998. Industry insiders had predicted P&G’s return to adult incontinence, a market that offers significantly more growth potential than similar absorbent markets.

The new line consists of liners, pads and underwear designed to offer comfort, protection and discretion, in a feminine design, that absorbs leaks and odors quickly. According to P&G, Always Discreet pads are up to 40% thinner than the leading brand and absorb twice as much fluid as women may need, based on the average consumer usage of incontinence products. The curve-hugging, disposable Always Discreet underwear is designed to be easy to wear and discreet, with the extra protection of Dual LeakGuard barriers to help stop leaks where they are most likely to occur.

P&G is building off the success of its Always feminine hygiene brand, which has provided protection for more than 30 years. With Always Discreet, the brand continues to support women in all phases of their lives with the comfort and protection they’ve come to expect from Always. According to sources familiar with incontinence trends, about 40% of current Always feminine hygiene customers use the products to handle incontinence problems.

“Always Discreet products have undergone extensive consumer testing and are specifically designed to provide the things that matter most to women with sensitive bladders, including odor neutralization protection and discretion,’’ said Chandrika Kasturi, Always Discreet product research director. “Our advanced OdorLock technology traps odors instantly and for hours and our innovative Advanced Core Technology absorbs fluids to the core and locks it away, offering incredible dryness protection.”

P&G began test marketing Always Discreet liners in the U.K. a few months ago and the hygiene industry has been speculating that a North American launch was imminent. The company exited the adult incontinence market, which it helped create in the 1970s, in 1999 when it sold its Attends brand to PaperPak Industries.

Adult incontinence growth

The news that P&G would reenter adult incontinence came as no surprise because of the high level of growth being seen in adult incontinence. During the last 15 years, roughly the amount of time P&G had been absent from the market—North American adult incontinence sales have tripled to reach $1.5 billion, according to experts. Global sales, now at $7 billion, are growing about 8.4% annually, faster than any other paper-based household products.

With an estimated 25 million Americans experiencing incontinence symptoms, manufacturers are coming up with more solutions to these products.

Traditionally, the market leader has been Kimberly-Clark with its Depend and Poise brands, and this company has been launching a steady stream of incontinence items including X.

Meanwhile, industry newcomer Butterfly brands has received laurels for its body liners, which meets the needs of sufferers of accidental bowel leakage (ABL). Last year at Vision, the company received an award for the product, which is being called a category creating innovation and is already meeting the needs of many ADL sufferers, a condition that affects about 20% of women over the age of 40.

While Butterfly brands and P&G are newcomers to adult incontinence, market veteran Kimberly-Clark has made numerous efforts to make sure this business meets the needs of as many people as possible. Recent product introductions or innovations have included male guards and better fitting adult diapers.

These efforts will surely pay off in the long, if not near, term. Already, there are signs that the adult incontinence market could challenge the disposable baby diaper market in terms of sales and volumes. Reports coming out of Japan indicate that adult diapers are outselling baby diapers, where nearly one in every four people is over 65 years old.

While the U.S. market is not quite as dominated by adult incontinence, INDA estimated that adult incontinence product sales will outpace boy baby diapers and feminine hygiene products with an annual growth rate of 3.5%.

Growth continues for nonwovens

Global demand for nonwovens is forecast to rise 5.3% annually to nine metric tons in 2017. However, there is a great deal of variation among different regions and countries, according to market research. Countries with well developed manufacturing sectors and a population with relatively high personal incomes, such as the U.S., Japan, and West European countries, have well established nonwovens markets. In these areas, nonwovens are prevalent in the production of a variety of goods, and individuals have the financial capability to purchase nonwoven-based consumer items.

Most experts agree that demand for nonwovens in developed countries is expected to accelerate from the pace set from 2007-2012, when recessionary conditions for most of the period brought outright declines in manufacturing and construction activity. Despite the acceleration, growth in nonwovens demand in developed areas will remain well below the global average as continued industrialization and increasing personal incomes in developing countries promote nonwovens demand.

Ongoing economic advances in China and other developing countries will promote the development of manufacturing sectors, providing opportunities for nonwovens in a variety of goods, such as filters. With respect to consumer goods, rising incomes and standards of living will propel individuals to purchase convenience items, promoting the production of disposable infant diapers among other items that are made with significant amounts of nonwoven fabrics. The largest regional market for nonwovens is the Asia Pacific region, with 39% of the global total. Two of the top three nonwovens consuming countries—China and Japan—are located in the region. Advances will be driven by China, which will account for 60% of the regional sales in 2017 and nearly 40% of additional global volume demand through 2017.