04.03.20

By Smithers

Five years ago, North America was the second-largest consumer of wetlaid nonwovens, accounting for 39.1% of the marketshare, following just short of Europe, which accounted for 41.5%. In 2020, North America will surpass Europe as global leader, with a market share of 43.8%.

In 2020, North America’s consumption will reach 265,600 tons, up from 172,700 tons in 2015 at a 9% CAGR. To put this into perspective, global consumption of all wetlaid nonwovens will reach 606,200 tons, approximately $1.8 billion in sales, according to the data presented in Smithers’ latest report, The Future of Wetlaid Nonwovens to 2025.

Globally, wetlaid nonwovens continue to suffer through some market issues, primarily substitution by spunlaid and other nonwovens, in some of the older, established markets but are participating in some of the newest nonwoven applications. In some growing markets, notably wipes and especially flushable wipes, wetlaid has an important and growing share.

Rest of World

Despite current trends for North America, by 2025, the region’s growth will slow as market share grows to 47.4% — a consumption 383,700 tons and a CAGR of 7.6%.

Europe falls to the second-largest consumer of wetlaid nonwovens in 2020, accounting for 36.9% of the market share and 223,700 tons in consumption. Due to economic and geopolitical issues, Europe’s growth will slow, with a CAGR at 3.5% and consumption of 265,300 tons in 2025.

Asia ranked in third place in 2015 and remains there in 2020, with a marketshare of 14.9% and consumption of 90,400 tons. Through 2025, Asia will see stable growth, spurred by China’s trade issues, while global economic growth slows slightly. Asia’s marketshare will increase to 15.7% and the region will consume approximately 127,500 tons in 2025. However, compound annual growth will remain at 7.1% during this time period.

Trends in Process Variants

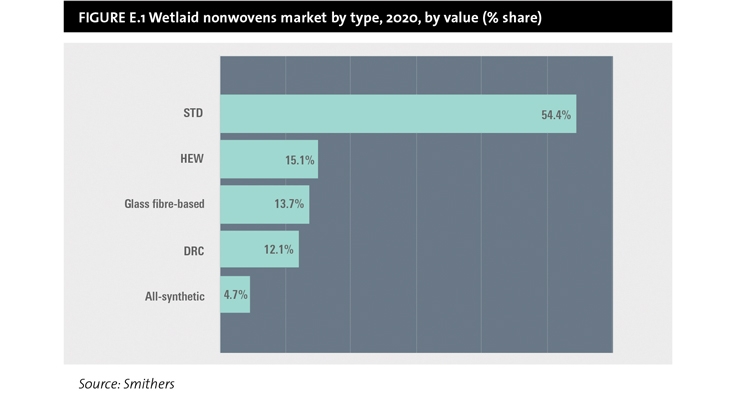

Wetlaid nonwovens remains one of the smallest of the major nonwovens processes, but it contains some important products and process variants. The largest variant by far is standard synthetic/pulp wetlaid, which accounts for about 54.4% of the value of all wetlaid in 2020. This variant will slowly lose market share, dropping to 51% in 2025.

Hydroentangled wetlaid is a product recently redefined as wetlaid and used primarily in flushable wipes. Hydroentangled wetlaid accounts for 15.1% of global wetlaid value in 2020; due to a capacity surplus and to fast-growing demand in flushable wipe end uses, its market share will increase to 17.9% by 2025.

Glass fiber-based wetlaid or wetlaid fiberglass accounts for about 13.7% of wetlaid nonwovens value in 2020; its share is growing and will account for 16% of the wetlaid market in 2025.

DRC, or double recrepe, is a special type of wetlaid, predominant in North America. DRC accounts for 12.1% of global wetlaid value in 2020; due to capacity limitations, its market share will decrease to 10.6% by 2025. The all-synthetic variant accounted for 4.7% in 2020, which decreases to 4.5% in 2025.

The Future of Wetlaid Nonwovens dives into the trends and challenges for the wetlaid nonwovens market to help industry leaders make the best decisions.

To learn more about The Future of Wetlaid Nonwovens to 2025, download the brochure at https://www.smithers.com/services/market-reports/nonwovens/wetlaid-nonwovens-to-2025.

Five years ago, North America was the second-largest consumer of wetlaid nonwovens, accounting for 39.1% of the marketshare, following just short of Europe, which accounted for 41.5%. In 2020, North America will surpass Europe as global leader, with a market share of 43.8%.

In 2020, North America’s consumption will reach 265,600 tons, up from 172,700 tons in 2015 at a 9% CAGR. To put this into perspective, global consumption of all wetlaid nonwovens will reach 606,200 tons, approximately $1.8 billion in sales, according to the data presented in Smithers’ latest report, The Future of Wetlaid Nonwovens to 2025.

Globally, wetlaid nonwovens continue to suffer through some market issues, primarily substitution by spunlaid and other nonwovens, in some of the older, established markets but are participating in some of the newest nonwoven applications. In some growing markets, notably wipes and especially flushable wipes, wetlaid has an important and growing share.

Rest of World

Despite current trends for North America, by 2025, the region’s growth will slow as market share grows to 47.4% — a consumption 383,700 tons and a CAGR of 7.6%.

Europe falls to the second-largest consumer of wetlaid nonwovens in 2020, accounting for 36.9% of the market share and 223,700 tons in consumption. Due to economic and geopolitical issues, Europe’s growth will slow, with a CAGR at 3.5% and consumption of 265,300 tons in 2025.

Asia ranked in third place in 2015 and remains there in 2020, with a marketshare of 14.9% and consumption of 90,400 tons. Through 2025, Asia will see stable growth, spurred by China’s trade issues, while global economic growth slows slightly. Asia’s marketshare will increase to 15.7% and the region will consume approximately 127,500 tons in 2025. However, compound annual growth will remain at 7.1% during this time period.

Trends in Process Variants

Wetlaid nonwovens remains one of the smallest of the major nonwovens processes, but it contains some important products and process variants. The largest variant by far is standard synthetic/pulp wetlaid, which accounts for about 54.4% of the value of all wetlaid in 2020. This variant will slowly lose market share, dropping to 51% in 2025.

Hydroentangled wetlaid is a product recently redefined as wetlaid and used primarily in flushable wipes. Hydroentangled wetlaid accounts for 15.1% of global wetlaid value in 2020; due to a capacity surplus and to fast-growing demand in flushable wipe end uses, its market share will increase to 17.9% by 2025.

Glass fiber-based wetlaid or wetlaid fiberglass accounts for about 13.7% of wetlaid nonwovens value in 2020; its share is growing and will account for 16% of the wetlaid market in 2025.

DRC, or double recrepe, is a special type of wetlaid, predominant in North America. DRC accounts for 12.1% of global wetlaid value in 2020; due to capacity limitations, its market share will decrease to 10.6% by 2025. The all-synthetic variant accounted for 4.7% in 2020, which decreases to 4.5% in 2025.

The Future of Wetlaid Nonwovens dives into the trends and challenges for the wetlaid nonwovens market to help industry leaders make the best decisions.

To learn more about The Future of Wetlaid Nonwovens to 2025, download the brochure at https://www.smithers.com/services/market-reports/nonwovens/wetlaid-nonwovens-to-2025.