11.07.16

In 2015 Cotton Incorporated requisitioned a study of the global feminine care market including pads, tampons and panytliners. Target markets were the U.S., China, Mexico and four countries in Europe (Italy, Germany, France and the U.K.). The study, in combination with Euromonitor data, sought to answer the who, what, where and why questions underlying this important disposable hygiene market. The methodology consisted of quantitative studies of 500-1000 feminine hygiene product users. Qualitative studies followed using focus groups with 24-26 users in the China and U.S. markets.

Market demographic data was collected relative to the female population using sanitary protection products, their product usage, brand loyalty, purchase drivers, key sources of consumer product information and retail channel shopping habits. Additionally, the study examined attitudes toward product composition including both manmade fibers and natural, cotton fibers. These factors were also characterized by age group segments including Gen Z, Millenials, Gen X and Boomers.

Market Dynamics

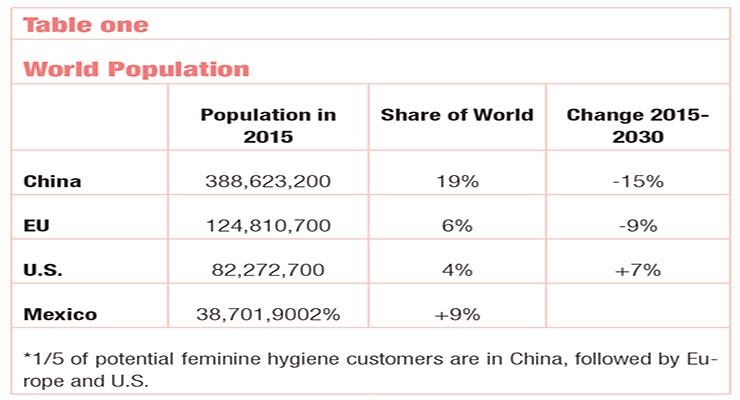

As of last year, China was home to the world’s largest feminine hygiene population of women ages 12-50 at 388,623,200 accounting for about 19% or one in five women in this category worldwide. This population, however, is expected to decline by 15% by 2030 due to China’s aging population and relatively low birth rate and is projected to be surpassed by India. The U.S. and Mexico will see modest growth in their populations in this group at 7% and 9% respectively while Europe will see a decline of 9%.

Today, the majority of women targeted by the feminine hygiene brands are the Millennial generation- ages 15-25 years. Millennials are as large a group as the Gen X and Boomers combined. In the future, Millenials and Gen Z population segments will account for almost the total feminine hygiene population.

Another important dynamic in benchmarking consumer preferences and purchase tendency is the underlying economic picture. China’s economy, as measured by GDP, is expected to double during this period from $ 11.3T to 20.8T but the US is expected to retain the highest GDP at $24.6T. Europe follows as the third largest economy with a GDP growth rate of 28% from $16.2 to $20.8T1.

Market penetration by feminine hygiene products is such, however, that the US has a commanding lead in market size with sales of pads, tampons and pantiliners ranging from 2x-6x the dollar value of other countries. The largest five-year growth rate is expected in Mexico at 16.8% supported by double digit growth across all three product types. Notably, panty liners appear to be generally on the decline across all countries except France.

Product Usage and Purchase Drivers

Feminine hygiene product usage by global consumers varies significantly by country, ethnicity, age and age segment, menstrual cycle phase and in change frequency. Regular pad share is highest in Italy at 75% and lowest in Germany where tampons are the product of choice at 63%. Conversely tampon use is very small in Mexico where nine in 10 women use either overnight pads (48%) or regular pads (46%). Regular pads and tampons are the products most often used in the U.S. (41%), the U.K. (44%) and France (47% and 37% respectively). Women frequently combine products during menstruation. A third of tampon users frequently add a pad for additional protection. Nearly half of tampon users in Italy (51%) and the U.S. (47%) indicate they add a pad when wearing a tampon.

Product selection differences are also associated with age group and ethnicity. Gen X women (44% vs. 38% for Millennial women) and Hispanics (47%) are more likely to primarily use regular pads. On the other hand, tampons are more likely to be used by Milliennial women (45% vs. 34 for Gen X women), Caucasians (45% vs. 32%) and women whose menstruation lasts five days or less (45% vs. 34% for women with menstruation lasting six or more days). U.S. African Americans (28% vs. 12%) are significantly more likely than other groups to wear overnight pads during menstruation.

Product usage differs by menstruation phase in all markets except Germany where tampons dominate. Night pads are the primary product form worn across markets (except Germany) during heavy nights, and in developing markets like China and Mexico pads and night pads dominate the market (tampon usage is extremely low). Women’s menstrual cycle on average lasts about five days and the number of products worn per cycle ranges from four to five per day; U.S. women average 25 products/month, Europe 23 and Mexico 21.4.

Another key finding is that all brands, particularly new brands face a tough challenge in driving market share growth. The challenge is not only high brand loyalty level but also is one of market domination by a small number of brands. About eight in 10 women generally stay with their chosen brand and the top three brands typically dominate their market. The top three brands in all countries account for eight of every 10 tampons sold, six out of 10 pads and seven out of 10 panty liners. While the majority of women in the U.S. and the U.K. are willing to switch brands for a better price, less than half are willing to do so in Germany, France, Italy and Mexico.

Purchase drivers can be grouped into three major categories; performance, comfort and price. Key product performance factors include leakage prevention, absorbency and skin dryness. Overall comfort includes softness, fit, and hypoallergenic qualities.

The relative priority of purchase drivers was examined according to primary product worn, country and age group, particularly with Gen X women. For most women, performance and comfort were more important than brand. This was particularly true for Mexican women who were more likely to say almost all performance and comfort factors were important. A stance of looking at more factors to discern value is common in developing markets where trust is an issue in the face of a constant stream of new products and brands. German women place a higher importance on discretion, which may account for their preference for tampons. U.S. pad users are more price sensitive than their European counterparts. Gen X women often had different top priorities than the average per product type and in all countries.

Studies conducted in the markets of Europe and Mexico additionally surveyed the needs and habits of girls ages 10-17. Several habits and attitudes stood out in Europe. This younger group was more interested in sustainability and voiced a higher level of unmet needs and social media use. They also were more interested in subscription services for product purchases to avoid embarrassment. Using social media as a tool to educate, generate interest, and build a brand relationship with young women is essential for any established brand or new entrant.

Product Information Sources

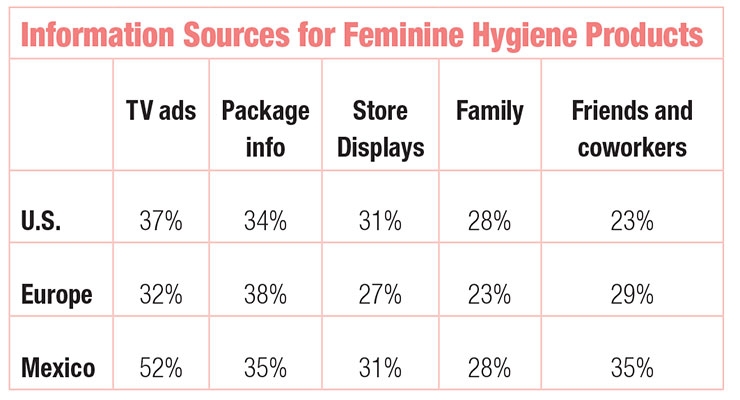

The feminine hygiene product information sources consulted by women were found to be scattered across TV ads, product packaging, store displays, family members and friends and coworkers. Mexican (52%) and U.S. (37%) women favor TV ads, while European women primarily (38%) rely upon product packaging for their product instruction. Social media, according to this study, is largely underutilized as a customer engagement tool as only 1 in 5 women say they follow feminine hygiene products on social media sites. Of those using social media, two out of 10 obtain information through feminine hygiene brand sites and 1 in 10 tap social media sites. U.S. women primarily use social media sites to track promotions and coupons.

Retail shopping channel preferences were obtained by using a combined average of pads, liners and tampons per country. The majority of women in China (87%), Italy (81%), France (76%) and the U.S. (57%) and the UK (51%) shop for their products at mass merchants. In contrast, 3 in 4 German women purchase their products at drug stores and seven in 10 Mexican women buy their products at grocery stores. Telegroup feedback indicated shopping choices were based on convenience, best prices or price-related best coupons, points and rewards.

Cotton Opportunities

This study also probed the perceptions of feminine hygiene product composition in terms of made-made versus natural fibers, namely cotton fibers. Nearly half of women in Europe (47%), about six in 10 in the U.S. (60%), and China (64%), and eight in 10 in Mexico say they believe that their feminine hygiene products are already made from cotton. In Europe, eight in 10 Italian women would prefer cotton products, followed by women in France (58%), the UK (49%), and Germany (45%).

When educated about the presence of manmade fibers in most feminine hygiene products used today, the majority of women expressed a level of concern. Women in the US (55%), Europe (66%) and Mexico (77%) said that they were bothered by the use of these fibers. This perception among those bothered translated into high levels of very or somewhat likely to avoid brands scores of 6 in 10 in the U.S. and Europe and eight in 10 in Mexico.

Once informed of the absence of cotton in these products, the majority of women in Mexico (94%), Europe (80%), China (76%), and the U.S. (66%) said they would be very interested in purchasing such products. In Europe, interest is strongest in Italy (91%), followed by the UK (77%), France (75%), and Germany (74%). Millennial-specific perceptions of cotton tracked closely with this data.

The strong interest in cotton products by a majority of women in the U.S., Europe, China and Mexico was based on their belief that cotton would perform better in terms of softness, comfort, breathability, being hypoallergenic and sustainable. Even with strong brand loyalty and price sensitivity in the global feminine hygiene market, the majority of women in Mexico (56%), China (52%) and a good portion in the U.S. (42%) and Europe (38%) are likely to purchase cotton products that are a different brand and slightly higher price. European girls ages 10-17 were even more likely to break their brand loyalty for the natural benefits of cotton.

Summary

Over the next 15 years economic growth is expected to accelerate in developing markets like China and Mexico and to remain moderate in the U.S. and Europe. Feminine hygiene sales are projected to see modest growth in the U.S. and more rapid growth in Mexico. The top three major brands of products account for more than 70% of sales worldwide and enjoy a high level of brand loyalty. This foothold makes it difficult to grow share both with established and new brands.

Purchase drivers and product usage habits vary significantly by country and age group. Global feminine hygiene companies appear to have opportunities for building share growth and consumer loyalty by addressing these differences. The younger 10-17 group in Europe, for example, stood out for their higher interest level in sustainability, greater level of unmet needs and frequent social media use. An opportunity also seems to exist in improving and extending digital customer outreach, with young Gen Z and Millennial age women. Not unexpectedly, however, price and performance remain important and can drive brand changes. This research indicates global interest in “natural” cotton fiber content in feminine hygiene products is high and is sharply contrasted to consumer perceptions of “man-made fibers."

Market demographic data was collected relative to the female population using sanitary protection products, their product usage, brand loyalty, purchase drivers, key sources of consumer product information and retail channel shopping habits. Additionally, the study examined attitudes toward product composition including both manmade fibers and natural, cotton fibers. These factors were also characterized by age group segments including Gen Z, Millenials, Gen X and Boomers.

Market Dynamics

As of last year, China was home to the world’s largest feminine hygiene population of women ages 12-50 at 388,623,200 accounting for about 19% or one in five women in this category worldwide. This population, however, is expected to decline by 15% by 2030 due to China’s aging population and relatively low birth rate and is projected to be surpassed by India. The U.S. and Mexico will see modest growth in their populations in this group at 7% and 9% respectively while Europe will see a decline of 9%.

Today, the majority of women targeted by the feminine hygiene brands are the Millennial generation- ages 15-25 years. Millennials are as large a group as the Gen X and Boomers combined. In the future, Millenials and Gen Z population segments will account for almost the total feminine hygiene population.

Another important dynamic in benchmarking consumer preferences and purchase tendency is the underlying economic picture. China’s economy, as measured by GDP, is expected to double during this period from $ 11.3T to 20.8T but the US is expected to retain the highest GDP at $24.6T. Europe follows as the third largest economy with a GDP growth rate of 28% from $16.2 to $20.8T1.

Market penetration by feminine hygiene products is such, however, that the US has a commanding lead in market size with sales of pads, tampons and pantiliners ranging from 2x-6x the dollar value of other countries. The largest five-year growth rate is expected in Mexico at 16.8% supported by double digit growth across all three product types. Notably, panty liners appear to be generally on the decline across all countries except France.

Product Usage and Purchase Drivers

Feminine hygiene product usage by global consumers varies significantly by country, ethnicity, age and age segment, menstrual cycle phase and in change frequency. Regular pad share is highest in Italy at 75% and lowest in Germany where tampons are the product of choice at 63%. Conversely tampon use is very small in Mexico where nine in 10 women use either overnight pads (48%) or regular pads (46%). Regular pads and tampons are the products most often used in the U.S. (41%), the U.K. (44%) and France (47% and 37% respectively). Women frequently combine products during menstruation. A third of tampon users frequently add a pad for additional protection. Nearly half of tampon users in Italy (51%) and the U.S. (47%) indicate they add a pad when wearing a tampon.

Product selection differences are also associated with age group and ethnicity. Gen X women (44% vs. 38% for Millennial women) and Hispanics (47%) are more likely to primarily use regular pads. On the other hand, tampons are more likely to be used by Milliennial women (45% vs. 34 for Gen X women), Caucasians (45% vs. 32%) and women whose menstruation lasts five days or less (45% vs. 34% for women with menstruation lasting six or more days). U.S. African Americans (28% vs. 12%) are significantly more likely than other groups to wear overnight pads during menstruation.

Product usage differs by menstruation phase in all markets except Germany where tampons dominate. Night pads are the primary product form worn across markets (except Germany) during heavy nights, and in developing markets like China and Mexico pads and night pads dominate the market (tampon usage is extremely low). Women’s menstrual cycle on average lasts about five days and the number of products worn per cycle ranges from four to five per day; U.S. women average 25 products/month, Europe 23 and Mexico 21.4.

Another key finding is that all brands, particularly new brands face a tough challenge in driving market share growth. The challenge is not only high brand loyalty level but also is one of market domination by a small number of brands. About eight in 10 women generally stay with their chosen brand and the top three brands typically dominate their market. The top three brands in all countries account for eight of every 10 tampons sold, six out of 10 pads and seven out of 10 panty liners. While the majority of women in the U.S. and the U.K. are willing to switch brands for a better price, less than half are willing to do so in Germany, France, Italy and Mexico.

Purchase drivers can be grouped into three major categories; performance, comfort and price. Key product performance factors include leakage prevention, absorbency and skin dryness. Overall comfort includes softness, fit, and hypoallergenic qualities.

The relative priority of purchase drivers was examined according to primary product worn, country and age group, particularly with Gen X women. For most women, performance and comfort were more important than brand. This was particularly true for Mexican women who were more likely to say almost all performance and comfort factors were important. A stance of looking at more factors to discern value is common in developing markets where trust is an issue in the face of a constant stream of new products and brands. German women place a higher importance on discretion, which may account for their preference for tampons. U.S. pad users are more price sensitive than their European counterparts. Gen X women often had different top priorities than the average per product type and in all countries.

Studies conducted in the markets of Europe and Mexico additionally surveyed the needs and habits of girls ages 10-17. Several habits and attitudes stood out in Europe. This younger group was more interested in sustainability and voiced a higher level of unmet needs and social media use. They also were more interested in subscription services for product purchases to avoid embarrassment. Using social media as a tool to educate, generate interest, and build a brand relationship with young women is essential for any established brand or new entrant.

Product Information Sources

The feminine hygiene product information sources consulted by women were found to be scattered across TV ads, product packaging, store displays, family members and friends and coworkers. Mexican (52%) and U.S. (37%) women favor TV ads, while European women primarily (38%) rely upon product packaging for their product instruction. Social media, according to this study, is largely underutilized as a customer engagement tool as only 1 in 5 women say they follow feminine hygiene products on social media sites. Of those using social media, two out of 10 obtain information through feminine hygiene brand sites and 1 in 10 tap social media sites. U.S. women primarily use social media sites to track promotions and coupons.

Retail shopping channel preferences were obtained by using a combined average of pads, liners and tampons per country. The majority of women in China (87%), Italy (81%), France (76%) and the U.S. (57%) and the UK (51%) shop for their products at mass merchants. In contrast, 3 in 4 German women purchase their products at drug stores and seven in 10 Mexican women buy their products at grocery stores. Telegroup feedback indicated shopping choices were based on convenience, best prices or price-related best coupons, points and rewards.

Cotton Opportunities

This study also probed the perceptions of feminine hygiene product composition in terms of made-made versus natural fibers, namely cotton fibers. Nearly half of women in Europe (47%), about six in 10 in the U.S. (60%), and China (64%), and eight in 10 in Mexico say they believe that their feminine hygiene products are already made from cotton. In Europe, eight in 10 Italian women would prefer cotton products, followed by women in France (58%), the UK (49%), and Germany (45%).

When educated about the presence of manmade fibers in most feminine hygiene products used today, the majority of women expressed a level of concern. Women in the US (55%), Europe (66%) and Mexico (77%) said that they were bothered by the use of these fibers. This perception among those bothered translated into high levels of very or somewhat likely to avoid brands scores of 6 in 10 in the U.S. and Europe and eight in 10 in Mexico.

Once informed of the absence of cotton in these products, the majority of women in Mexico (94%), Europe (80%), China (76%), and the U.S. (66%) said they would be very interested in purchasing such products. In Europe, interest is strongest in Italy (91%), followed by the UK (77%), France (75%), and Germany (74%). Millennial-specific perceptions of cotton tracked closely with this data.

The strong interest in cotton products by a majority of women in the U.S., Europe, China and Mexico was based on their belief that cotton would perform better in terms of softness, comfort, breathability, being hypoallergenic and sustainable. Even with strong brand loyalty and price sensitivity in the global feminine hygiene market, the majority of women in Mexico (56%), China (52%) and a good portion in the U.S. (42%) and Europe (38%) are likely to purchase cotton products that are a different brand and slightly higher price. European girls ages 10-17 were even more likely to break their brand loyalty for the natural benefits of cotton.

Summary

Over the next 15 years economic growth is expected to accelerate in developing markets like China and Mexico and to remain moderate in the U.S. and Europe. Feminine hygiene sales are projected to see modest growth in the U.S. and more rapid growth in Mexico. The top three major brands of products account for more than 70% of sales worldwide and enjoy a high level of brand loyalty. This foothold makes it difficult to grow share both with established and new brands.

Purchase drivers and product usage habits vary significantly by country and age group. Global feminine hygiene companies appear to have opportunities for building share growth and consumer loyalty by addressing these differences. The younger 10-17 group in Europe, for example, stood out for their higher interest level in sustainability, greater level of unmet needs and frequent social media use. An opportunity also seems to exist in improving and extending digital customer outreach, with young Gen Z and Millennial age women. Not unexpectedly, however, price and performance remain important and can drive brand changes. This research indicates global interest in “natural” cotton fiber content in feminine hygiene products is high and is sharply contrasted to consumer perceptions of “man-made fibers."