Karen McIntyre, Senior Editor02.18.14

How quickly will new capacity be absorbed? This is the question on the minds of everyone doing business in spunmelt and spunbond, a market that has seen unprecedented investment during the past five years. The combined capacity of the many new lines that have either recently come onstream or are currently under construction is estimated above 500,000 tons. Experts disagree on exactly how long it will take for all of this capacity to be absorbed by the industry, but all agree that competition has intensified within the market for spunmelt nonwovens.

“I believe in general and especially for non hygiene applications an oversupply situation exists for polypropylene spunbond,” says Serkan Gogus, commercial director of Mogul Nonwovens, Gaziantep, Turkey. “There are continuous investments and old lines which can’t sell hygiene so unless there’s a large increase in demand this doesn’t seem likely to change.”

Mikael Staal Axelsen, CEO of Fibertex Personal Care is more optimistic. His company makes spunmelt nonwovens in Denmark and Malaysia and is currently adding a fourth line in Malaysia in response to growth in the region.

“There is a slight oversupply in Europe and this will probably remain as growth rates are low,” says Axelsen. “There is bigger over supply in the Middle East and Africa but the growth rates will absorb eventually. Asia is oversupplied and will take two to three years to absorb.”

While the bulk of capacity announced in recent years has come onstream, more is rolling out and will continue to move into the operational stage in the next 12 months or so. And, some investments—like Fitesa’s commitment to investing $50 million in the U.S. and globally—continue to be announced, although experts predict these will soon run dry, if they haven’t already.

“We went through the announcement phase and now we are in the installation and operation/commissioning stage,” says David Price, principal of Price Hanna consultants. “The absorption stage will take some time depending on whether or not older assets will be retired.”

So far few older lines have been mothballed and instead are being repurposed to meet the specifications of markets outside of the hygiene market while the new lines offer the high efficiencies and thinner products required by the hygiene market.

“The old machines can be cost competitive in certain markets but they will eventually be targeted at industrial markets,” Price says.

Around the world

Investment in the spunmelt market has been truly global in its scope in recent years with new lines popping up in markets with established nonwovens industries like North America or Europe but also in countries that have never before seen western machinery lines like Peru and Indonesia. Of particular interest has been China where new lines have been added by western companies like Avgol, PGI and First Quality Nonwovens as well as Chinese and Asian producers like Toray, Jofo Enterprises and Mitsui Chemical.

“Investments—mainly in China but also in Japan, Thailand, Malaysia and Indonesia—have increased capacity beyond demand,” Axelsen says. “Currently there is an overcapacity versus demand of around 20% in Asia Pacific for hygiene applications. The market is, however growing and with no further investments than those completed or announced, we should see a balance in 2016-2017.”

Based in Denmark, Fibertex has opted to expand into Asia via Malaysia where its output will reach 70,000 tons later this year when a fourth line is complete. This output primarily serves the entire Asian continent, Axelsen says.

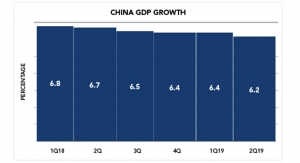

Within Asia, growth is being driven by growing demand for baby diapers as more consumers reach the disposable income levels necessary to use these products. Additionally, growth is expected following the Chinese government’s decision in late 2013 to relax the one child per family ruling, which should significantly boost the country’s birth rate.

Beyond China, investment has been aggressive in Southeast Asia. Toray Advance Materials, a Korean company that has ambitiously expanded in China in recent years, started making spunmelt nonwovens in Indonesia last year, and a number of Japanese companies, including Mitsui Chemicals, Asahi Kasei and Unitika have established sites in Thailand.

“The hygiene market has become much more sophisticated in China and the rest of Asia and more people are using western technology,” Price says. “There are still a lot of Chinese lines around but they are designed to meet very market-specific needs.”

Trailing only slightly behind Asia in investments is the Middle East and North Africa region, which is proving to be valued not only for its central location but also its easy access to raw material suppliers. In recent years, countries like Turkey, Saudi Arabia and, most recently, Egypt have emerged as important nonwovens producers and spunmelt has been a top choice for nonwovens producers looking to capture hygiene growth in emerging markets.

Two major Saudi producers, Saudi German Nonwovens and Saudi Arabia Advanced Fabrics (SAAF) last year established large-scale operations on the west coast of Saudi Arabia, which provides better logistics for shipping westward than their original sites on the east coast of the nation.

“Before we added the new line, nearly half of our output had to be transported nearly 1,000 miles across the Saudi desert to reach the seaport at Jeddah,” says SGN spokesman Richard Gillings. “It was a strategic decision to add a site on the west coast of Saudi Arabia for easier shipping logistics.”

While the establishment of these operations has made logistics easier, now the companies are both waiting for a more balanced supply and demand picture in the market before considering further investment.

“There will be no expansion now but we are looking at the future,” says SAAF managing director Mounir Haddad. “The new site on the west coast of Saudi Arabia has the potential to house more lines. It opens up opportunities in Egypt where a lot of companies are investing and we can see that opportunities in the medical market will soon increase in Europe.”

Egypt is one of the countries that is new to nonwovens investment. In 2011, two companies, Czech Republic’s Pegas and Turkey’s Gulsan both announced they would add spunmelt operations there to target growth in North Africa and those lines are now starting commercial production. These lines will meet demand for growth in the region, where multinationals like Procter & Gamble and Unicharm have already invested.

Alican Yilankirkan, commercial director of Turkish company General Nonwovens, reports supply outweighing demand in the current market. This company, which recently doubled the size of its operation, makes spunbond and air through bonded nonwovens supplying Turkey, the Middle East and Europe.

“In the current market situation, the supply is higher then demand which makes the competition on quality, service, delivery and pricing,” Yilankirkan says. “The oversupply in Europe still seems to exist and the unstable situation in some Middle East countries also makes it difficult to divert some excess capacity to this region.”

Also in Turkey, Mogul recently started producing a new core/sheath type bicomponent line, which followed a new polyester spunbond line. The new line brings the total polyester capacity for Mogul to 15,000 tons, making it one of the key players in the pet spunbond market. The new bico pet line will provide area thermal bonded flat fabrics in round and tiptrilobal filament shapes in low denier..

Beyond, the developing market investment has continued in North America with new lines up and running at Avgol in North Carolina, PGI in Virginia and Fitesa and Companhia Providencia in South Carolina as well as in South America where Fitesa has added new lines in Brazil and Peru, Providencia has expanded in Brazil and PGI continues to run sizable operations in Mexico, Argentina and Colombia.

Investment in Europe has been lighter. New lines from Union Industries, Fibertex and Fiberweb (now owned by Fitesa) came onstream in 2010, significantly adding to the continent’s capacity but since then most companies have shied away from significant investments. This has created a more balanced supply in this market, which, unlike North America has a number of smaller producers.

According to Allessandro Mottes, sales manager of Texbond, the market is difficult to predict in Europe. While adult incontinence growth has been positive and hygiene companies are using more spunmelt per product, the growth will have to be robust in the next couple of years before supply and demand will balance out.

However, Mottes says he sees relief in areas outside of the hygiene market. “Spunmelt continues to be the best solution in an increasing number of applications,” he says. “Even in Western or South Europe, areas of little manufacturing development we find every day the possibility of introducing our webs into new processes or products.”

New technologies

The reasons behind the surge in new capacity in the spunmelt market are two-fold. On one hand it has been in advance of predicted significant growth in the hygiene market—baby diapers in developing nations and adult incontinence in more developed areas—but on the other hand these new lines also meet the need for more efficient lines that can produce thinner products without sacrificing integrity and quality. During the past decades common weights in spunbond and spunmelt nonwovens have decreased from 13-15 gsm all the way down to eight and some say materials could even get thinner.

“To be competitive, manufacturers had to upgrade their assets,” SAAF’s Haddad says. “The market is moving toward lighter products and you can’t get to those really low weights with the older lines.”

To achieve these low weights and high efficiencies, most manufacturers are relying on the technology of Reifenhauser’s Reicofil technology, which is continuously being improved upon and has become the preferred technology for hygiene applications.

“Reicofil is broad-based but designed particularly well for the hygiene market and they certainly hold a large marketshare when it comes to fine fiber polypropylene spunbond,” says Price.

While recent generations of the Reicofil technology are generally replacing earlier versions of the same technology, this technology first helped spunbond take share away from competing nonwovens technologies, like thermal bonded, in the hygiene market.

Still nonwovens manufacturers assert that Reicofil technology is only a launch pad for high quality products. Nonwovens makers add their own proprietary technology to set themselves apart from competition.

“The demand is always for a solution and materials represent only a part of it,” says Mottes. “Spunmelts have gone thinner and thinner without reducing performances and proved to be the best solution in almost every part of the diaper. To capture additional demand, makers of spunmelt should build on bulkiness, not to mention elasticity.”

Hills, Inc. specializes in using proprietary technology and processing knowledge to develop fiber- and fabric-based technologies for its clients’ needs. The confidential nature of these projects means many of these breakthroughs are never publicly disclosed but a set of technologies referred to as “Lofty Spunbond” is an internal Hills program under development to achieve the common goals expressed by diverse industries—customizable nonwoven densities utilizing the spunbond process.

The high-speed spunbond process ensures high-throughput production in a modest footprint. A low-energy thermal activation process (lofting) activates a spunlaid web causing it to “selfbond,” increase volume and/or become “elastic like.” The interlocking of the fibers in the nonwoven structure means no further bonding process is required after activation, eliminating the need for the more conventional calender or costly needleloom in some applications.

By varying the ratio and/or polymers in a multi-component fiber cross section, it is possible to tailor the resulting density. Heavier basis weights are ideal for lofty product requirements. The same equipment can produce a wide range of densities from well over 100 kg/m3 to less than 10 kg/m3. Continued development in this area focuses on even lower densities for certain applications.

Lower basis weight examples yield fabrics with elastic properties. The elasticity results from the crimped nature of the filaments within the nonwoven structure. The continuous filament nature of spunbond means the fibers cannot reorient within the fabric as with carded fabrics yielding both improved strength and resiliency. The elimination of any elastic polymers reduces cost and options for re-processing after use disposal.

The process may be implemented entirely inline where the activation immediately follows the fabric formation step conserving both space and efficiency. The flexibility of the process allows for separating the formation and activation into two steps where forming the high-loft final product closer to its point of use reduces shipping costs.

“I believe in general and especially for non hygiene applications an oversupply situation exists for polypropylene spunbond,” says Serkan Gogus, commercial director of Mogul Nonwovens, Gaziantep, Turkey. “There are continuous investments and old lines which can’t sell hygiene so unless there’s a large increase in demand this doesn’t seem likely to change.”

Mikael Staal Axelsen, CEO of Fibertex Personal Care is more optimistic. His company makes spunmelt nonwovens in Denmark and Malaysia and is currently adding a fourth line in Malaysia in response to growth in the region.

“There is a slight oversupply in Europe and this will probably remain as growth rates are low,” says Axelsen. “There is bigger over supply in the Middle East and Africa but the growth rates will absorb eventually. Asia is oversupplied and will take two to three years to absorb.”

While the bulk of capacity announced in recent years has come onstream, more is rolling out and will continue to move into the operational stage in the next 12 months or so. And, some investments—like Fitesa’s commitment to investing $50 million in the U.S. and globally—continue to be announced, although experts predict these will soon run dry, if they haven’t already.

“We went through the announcement phase and now we are in the installation and operation/commissioning stage,” says David Price, principal of Price Hanna consultants. “The absorption stage will take some time depending on whether or not older assets will be retired.”

So far few older lines have been mothballed and instead are being repurposed to meet the specifications of markets outside of the hygiene market while the new lines offer the high efficiencies and thinner products required by the hygiene market.

“The old machines can be cost competitive in certain markets but they will eventually be targeted at industrial markets,” Price says.

Around the world

Investment in the spunmelt market has been truly global in its scope in recent years with new lines popping up in markets with established nonwovens industries like North America or Europe but also in countries that have never before seen western machinery lines like Peru and Indonesia. Of particular interest has been China where new lines have been added by western companies like Avgol, PGI and First Quality Nonwovens as well as Chinese and Asian producers like Toray, Jofo Enterprises and Mitsui Chemical.

“Investments—mainly in China but also in Japan, Thailand, Malaysia and Indonesia—have increased capacity beyond demand,” Axelsen says. “Currently there is an overcapacity versus demand of around 20% in Asia Pacific for hygiene applications. The market is, however growing and with no further investments than those completed or announced, we should see a balance in 2016-2017.”

Based in Denmark, Fibertex has opted to expand into Asia via Malaysia where its output will reach 70,000 tons later this year when a fourth line is complete. This output primarily serves the entire Asian continent, Axelsen says.

Within Asia, growth is being driven by growing demand for baby diapers as more consumers reach the disposable income levels necessary to use these products. Additionally, growth is expected following the Chinese government’s decision in late 2013 to relax the one child per family ruling, which should significantly boost the country’s birth rate.

Beyond China, investment has been aggressive in Southeast Asia. Toray Advance Materials, a Korean company that has ambitiously expanded in China in recent years, started making spunmelt nonwovens in Indonesia last year, and a number of Japanese companies, including Mitsui Chemicals, Asahi Kasei and Unitika have established sites in Thailand.

“The hygiene market has become much more sophisticated in China and the rest of Asia and more people are using western technology,” Price says. “There are still a lot of Chinese lines around but they are designed to meet very market-specific needs.”

Trailing only slightly behind Asia in investments is the Middle East and North Africa region, which is proving to be valued not only for its central location but also its easy access to raw material suppliers. In recent years, countries like Turkey, Saudi Arabia and, most recently, Egypt have emerged as important nonwovens producers and spunmelt has been a top choice for nonwovens producers looking to capture hygiene growth in emerging markets.

Two major Saudi producers, Saudi German Nonwovens and Saudi Arabia Advanced Fabrics (SAAF) last year established large-scale operations on the west coast of Saudi Arabia, which provides better logistics for shipping westward than their original sites on the east coast of the nation.

“Before we added the new line, nearly half of our output had to be transported nearly 1,000 miles across the Saudi desert to reach the seaport at Jeddah,” says SGN spokesman Richard Gillings. “It was a strategic decision to add a site on the west coast of Saudi Arabia for easier shipping logistics.”

While the establishment of these operations has made logistics easier, now the companies are both waiting for a more balanced supply and demand picture in the market before considering further investment.

“There will be no expansion now but we are looking at the future,” says SAAF managing director Mounir Haddad. “The new site on the west coast of Saudi Arabia has the potential to house more lines. It opens up opportunities in Egypt where a lot of companies are investing and we can see that opportunities in the medical market will soon increase in Europe.”

Egypt is one of the countries that is new to nonwovens investment. In 2011, two companies, Czech Republic’s Pegas and Turkey’s Gulsan both announced they would add spunmelt operations there to target growth in North Africa and those lines are now starting commercial production. These lines will meet demand for growth in the region, where multinationals like Procter & Gamble and Unicharm have already invested.

Alican Yilankirkan, commercial director of Turkish company General Nonwovens, reports supply outweighing demand in the current market. This company, which recently doubled the size of its operation, makes spunbond and air through bonded nonwovens supplying Turkey, the Middle East and Europe.

“In the current market situation, the supply is higher then demand which makes the competition on quality, service, delivery and pricing,” Yilankirkan says. “The oversupply in Europe still seems to exist and the unstable situation in some Middle East countries also makes it difficult to divert some excess capacity to this region.”

Also in Turkey, Mogul recently started producing a new core/sheath type bicomponent line, which followed a new polyester spunbond line. The new line brings the total polyester capacity for Mogul to 15,000 tons, making it one of the key players in the pet spunbond market. The new bico pet line will provide area thermal bonded flat fabrics in round and tiptrilobal filament shapes in low denier..

Beyond, the developing market investment has continued in North America with new lines up and running at Avgol in North Carolina, PGI in Virginia and Fitesa and Companhia Providencia in South Carolina as well as in South America where Fitesa has added new lines in Brazil and Peru, Providencia has expanded in Brazil and PGI continues to run sizable operations in Mexico, Argentina and Colombia.

Investment in Europe has been lighter. New lines from Union Industries, Fibertex and Fiberweb (now owned by Fitesa) came onstream in 2010, significantly adding to the continent’s capacity but since then most companies have shied away from significant investments. This has created a more balanced supply in this market, which, unlike North America has a number of smaller producers.

According to Allessandro Mottes, sales manager of Texbond, the market is difficult to predict in Europe. While adult incontinence growth has been positive and hygiene companies are using more spunmelt per product, the growth will have to be robust in the next couple of years before supply and demand will balance out.

However, Mottes says he sees relief in areas outside of the hygiene market. “Spunmelt continues to be the best solution in an increasing number of applications,” he says. “Even in Western or South Europe, areas of little manufacturing development we find every day the possibility of introducing our webs into new processes or products.”

New technologies

The reasons behind the surge in new capacity in the spunmelt market are two-fold. On one hand it has been in advance of predicted significant growth in the hygiene market—baby diapers in developing nations and adult incontinence in more developed areas—but on the other hand these new lines also meet the need for more efficient lines that can produce thinner products without sacrificing integrity and quality. During the past decades common weights in spunbond and spunmelt nonwovens have decreased from 13-15 gsm all the way down to eight and some say materials could even get thinner.

“To be competitive, manufacturers had to upgrade their assets,” SAAF’s Haddad says. “The market is moving toward lighter products and you can’t get to those really low weights with the older lines.”

To achieve these low weights and high efficiencies, most manufacturers are relying on the technology of Reifenhauser’s Reicofil technology, which is continuously being improved upon and has become the preferred technology for hygiene applications.

“Reicofil is broad-based but designed particularly well for the hygiene market and they certainly hold a large marketshare when it comes to fine fiber polypropylene spunbond,” says Price.

While recent generations of the Reicofil technology are generally replacing earlier versions of the same technology, this technology first helped spunbond take share away from competing nonwovens technologies, like thermal bonded, in the hygiene market.

Still nonwovens manufacturers assert that Reicofil technology is only a launch pad for high quality products. Nonwovens makers add their own proprietary technology to set themselves apart from competition.

“The demand is always for a solution and materials represent only a part of it,” says Mottes. “Spunmelts have gone thinner and thinner without reducing performances and proved to be the best solution in almost every part of the diaper. To capture additional demand, makers of spunmelt should build on bulkiness, not to mention elasticity.”

Hills, Inc. specializes in using proprietary technology and processing knowledge to develop fiber- and fabric-based technologies for its clients’ needs. The confidential nature of these projects means many of these breakthroughs are never publicly disclosed but a set of technologies referred to as “Lofty Spunbond” is an internal Hills program under development to achieve the common goals expressed by diverse industries—customizable nonwoven densities utilizing the spunbond process.

The high-speed spunbond process ensures high-throughput production in a modest footprint. A low-energy thermal activation process (lofting) activates a spunlaid web causing it to “selfbond,” increase volume and/or become “elastic like.” The interlocking of the fibers in the nonwoven structure means no further bonding process is required after activation, eliminating the need for the more conventional calender or costly needleloom in some applications.

By varying the ratio and/or polymers in a multi-component fiber cross section, it is possible to tailor the resulting density. Heavier basis weights are ideal for lofty product requirements. The same equipment can produce a wide range of densities from well over 100 kg/m3 to less than 10 kg/m3. Continued development in this area focuses on even lower densities for certain applications.

Lower basis weight examples yield fabrics with elastic properties. The elasticity results from the crimped nature of the filaments within the nonwoven structure. The continuous filament nature of spunbond means the fibers cannot reorient within the fabric as with carded fabrics yielding both improved strength and resiliency. The elimination of any elastic polymers reduces cost and options for re-processing after use disposal.

The process may be implemented entirely inline where the activation immediately follows the fabric formation step conserving both space and efficiency. The flexibility of the process allows for separating the formation and activation into two steps where forming the high-loft final product closer to its point of use reduces shipping costs.