04.01.21

By Ian Bell

Filip Hoffmann-Häußler and Liying Qian, Euromonitor International

It goes without saying that Covid-19 ushered in something of a paradigm shift in consumers’ approach to home care and domestic cleaning. Where pre-pandemic the industry had struggled to engage, educate, and convince consumers to trade up, ‘threat’ arrived, and backed by government campaigns saw money, time and the breadth of domestic cleaning expand.

An illustration of the significance of this change can be found in everyday items, like touch screens, commonly found in public locations like retail stores and fast food outlets. These items once seemed like a good idea, easy to access and convenient, but is that still the case in 2021?

Door handles too, a mechanism to enter a room which came with little consideration for most, now the potential harborer of all manner of nasties which probably needs a clean. Not many felt the need to clean door handles before 2020 yet now it seems more apparent, something we could/should be doing, whether we actually do it or not.

Home Care Responds Strongly to Rapidly Changing Environment

Globally, surface care, dish care and toilet care all benefitted from a combination of lockdown, more time at home and the aforementioned elevated level of threat felt by many households. Home care cleaning wipes in particular responded well to the pandemic, offering no compromise disposable hygiene at a premium price point.

This is even more interesting given that the category had found itself in something of a cul de sac pre-pandemic, arguably seen as wasteful and definitely counter to the green/sustainability trend which has been gathering pace more generally but also observed crossing over into mainstream brand thinking and wider corporate identity.

A New High for Home Care

Disposable Hygiene that Lacks Breadth

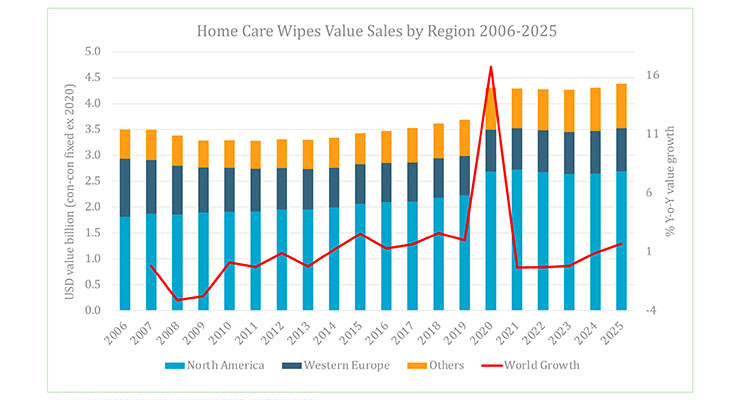

Total world home care wipe (including floor cleaning systems) value sales were worth $4.5 billion in 2020, growing 9% over 2019, meaning an additional $500 million of incremental value growth. This represents the most rapid growth seen in more than a decade since the category was shiny and new and in the pomp of its rapid growth phase.

Fundamentally however, although we can point to consumers around the world buying into wipes as a consequence of the pandemic, strong growth must be viewed in the context of surface care overall experiencing a 15% value sales uplift over the same period. As ever, any consideration of wipes is heavily related to income which translated into accessibility and affordability.

On the other side of the coin, ‘old school’ cleaning stalwart bleach also had a bumper year in 2020. By being cheap, flexible, broadly accessible and ultra-effective, bleach became a Covid cleaning response for the masses. Still in 2020, 81% of global home care wipes value (including floor cleaning systems) is found in just two regions, North America (62%) and Western Europe (19%).

Opportunities Further Afield and Competition at Home

For many Asian and Latin American consumers, the pandemic ushered in new ways of cleaning. In 2020, Unilever released Indonesia’s first all-purpose surface disinfecting wipes under the Wipol Power Clean brand, while Coperalcool in Brazil launched the nation’s first disposable disinfecting wipes. Growth in Asia and Latin America suggests there is still the opportunity for brands to develop a broader and more global market, the fact of the matter is the category is still a ‘top of the pyramid’ product, a fact that will not change any time soon.

While consolidated sales in developed regions are fantastic news in terms of distribution and route to consumer, it does come with developed market problems. In a commercial sense this could be represented by contract manufacturing and strong retailers driving private label alternatives to brands. That would very likely have been a central discussion point five years ago but the environment has changed, and this is not solely due to Covid-19.

Sustainability Concerns Bring Ingredient Choices and Labelling into the Spotlight

Sustainability was on the back burner at the height of the pandemic as households prioritized safety and hygiene, meaning that households have rarely used more energy, more chemical and any other resource required to achieve the desired result. As we move through the new normal and hopefully out of the pandemic phase, sustainability will emerge front and center for home care items meaning that wipes must either adapt to environment or somehow earn themselves a ‘pass’ in the mind of the regulator, brands and consumers.

Looking at leading brands, all have developed plastic policies in relation to their businesses which will inevitably drive change for the wipes industry longer term. Packaging will move from canister to flexible. Non-plastic substrates will see more interest as brands look to meet their 2025 and 2030 sustainability commitments. Be under no doubt, from laundry to toilet care, all categories will be under scrutiny when it comes to plastic usage per use and corporate polices will be driven through the supply chain in the search for solutions and greater levels of reduction. Wipes as a significant income generator for the industry, with high margins, will inevitably ask uncomfortable questions about commitment to the cause.

Stricter Regulation to Come Outside of Corporate Policy

In Europe there are moves to tighten regulations around single use plastics. For the author, single use plastics are items like soft drink bottles, but the coming legislation takes a much broader view including wipes (depending on the substrate) also as a single use plastic item. This is where it gets interesting. Legislation will not apply to commercial cleaning, at least part of the thinking here is that commercial cleaners have training and dispose of wipes appropriately. To this end, legislation is not about use of plastic per se but is more focused on how they are disposed. This is where we see strategy gaps beyond the impending more stringent approach to product labelling and directions for proper disposal.

Legislators have used beach litter collection data to designate wipes as a problem. Also, wipes continue to find their way into the sewage systems, meaning consumers (at least a group of them) are not following disposal guidelines correctly. Legislators are also pushed by utilities who point to wipes blocking drains and filters and also contributing to the ever-present menace of ‘fatbergs.’

Consumers for their part have seen wipes as a hygiene solution in a time of crisis but the brands who are buys ‘making hay while the sun shines’ have largely failed to support extended wipes usage with campaigns promoting responsible disposal. These are the same brands who are (for the most part) locked into long term plastic reduction commitments.

Responsible Disposal a Key Objective

In the U.S., regulating the disposal of wipes remains a largely state-led effort, with proper labelling practices at the center of the debate. Wipes claiming to be flushable are under increasing pressure to inform and educate consumers with correct and prominent labelling. Washington state set a yardstick for measuring clear labelling by being the first state to legally mandate “do not flush” claim for non-flushable disposable wipes.

Though the prospect of reaching a nationwide sweeping rule remains unclear, ongoing progress does not go unnoticed. In December, Responsible Flushing Alliance, a coalition of trade associations, wipes manufacturers and non-profits, was formed to raise consumer awareness about the proper disposal of non-flushable products, and to start, it has partnered with the California Association of Sanitation Agencies to develop an education campaign in California.

Something’s Got to Give

In conclusion, Euromonitor continues to see a long-term future for home care wipes, as the pandemic has helped to reinforce this in the mind of the consumer. There is also evidence that there is further growth outside of the core North America and European regions. That said, while wipes fundamentally offer convenience, they are also increasingly operating in a very complex environment and are being pulled by often opposing forces which is producing strategy gaps that need to be addressed. The spectre of further regulation while being ever-present is nothing new, but can we really say the same about the operating environment that will exist beyond the pandemic?

Filip Hoffmann-Häußler and Liying Qian, Euromonitor International

It goes without saying that Covid-19 ushered in something of a paradigm shift in consumers’ approach to home care and domestic cleaning. Where pre-pandemic the industry had struggled to engage, educate, and convince consumers to trade up, ‘threat’ arrived, and backed by government campaigns saw money, time and the breadth of domestic cleaning expand.

An illustration of the significance of this change can be found in everyday items, like touch screens, commonly found in public locations like retail stores and fast food outlets. These items once seemed like a good idea, easy to access and convenient, but is that still the case in 2021?

Door handles too, a mechanism to enter a room which came with little consideration for most, now the potential harborer of all manner of nasties which probably needs a clean. Not many felt the need to clean door handles before 2020 yet now it seems more apparent, something we could/should be doing, whether we actually do it or not.

Home Care Responds Strongly to Rapidly Changing Environment

Globally, surface care, dish care and toilet care all benefitted from a combination of lockdown, more time at home and the aforementioned elevated level of threat felt by many households. Home care cleaning wipes in particular responded well to the pandemic, offering no compromise disposable hygiene at a premium price point.

This is even more interesting given that the category had found itself in something of a cul de sac pre-pandemic, arguably seen as wasteful and definitely counter to the green/sustainability trend which has been gathering pace more generally but also observed crossing over into mainstream brand thinking and wider corporate identity.

A New High for Home Care

Disposable Hygiene that Lacks Breadth

Total world home care wipe (including floor cleaning systems) value sales were worth $4.5 billion in 2020, growing 9% over 2019, meaning an additional $500 million of incremental value growth. This represents the most rapid growth seen in more than a decade since the category was shiny and new and in the pomp of its rapid growth phase.

Fundamentally however, although we can point to consumers around the world buying into wipes as a consequence of the pandemic, strong growth must be viewed in the context of surface care overall experiencing a 15% value sales uplift over the same period. As ever, any consideration of wipes is heavily related to income which translated into accessibility and affordability.

On the other side of the coin, ‘old school’ cleaning stalwart bleach also had a bumper year in 2020. By being cheap, flexible, broadly accessible and ultra-effective, bleach became a Covid cleaning response for the masses. Still in 2020, 81% of global home care wipes value (including floor cleaning systems) is found in just two regions, North America (62%) and Western Europe (19%).

Opportunities Further Afield and Competition at Home

For many Asian and Latin American consumers, the pandemic ushered in new ways of cleaning. In 2020, Unilever released Indonesia’s first all-purpose surface disinfecting wipes under the Wipol Power Clean brand, while Coperalcool in Brazil launched the nation’s first disposable disinfecting wipes. Growth in Asia and Latin America suggests there is still the opportunity for brands to develop a broader and more global market, the fact of the matter is the category is still a ‘top of the pyramid’ product, a fact that will not change any time soon.

While consolidated sales in developed regions are fantastic news in terms of distribution and route to consumer, it does come with developed market problems. In a commercial sense this could be represented by contract manufacturing and strong retailers driving private label alternatives to brands. That would very likely have been a central discussion point five years ago but the environment has changed, and this is not solely due to Covid-19.

Sustainability Concerns Bring Ingredient Choices and Labelling into the Spotlight

Sustainability was on the back burner at the height of the pandemic as households prioritized safety and hygiene, meaning that households have rarely used more energy, more chemical and any other resource required to achieve the desired result. As we move through the new normal and hopefully out of the pandemic phase, sustainability will emerge front and center for home care items meaning that wipes must either adapt to environment or somehow earn themselves a ‘pass’ in the mind of the regulator, brands and consumers.

Looking at leading brands, all have developed plastic policies in relation to their businesses which will inevitably drive change for the wipes industry longer term. Packaging will move from canister to flexible. Non-plastic substrates will see more interest as brands look to meet their 2025 and 2030 sustainability commitments. Be under no doubt, from laundry to toilet care, all categories will be under scrutiny when it comes to plastic usage per use and corporate polices will be driven through the supply chain in the search for solutions and greater levels of reduction. Wipes as a significant income generator for the industry, with high margins, will inevitably ask uncomfortable questions about commitment to the cause.

Stricter Regulation to Come Outside of Corporate Policy

In Europe there are moves to tighten regulations around single use plastics. For the author, single use plastics are items like soft drink bottles, but the coming legislation takes a much broader view including wipes (depending on the substrate) also as a single use plastic item. This is where it gets interesting. Legislation will not apply to commercial cleaning, at least part of the thinking here is that commercial cleaners have training and dispose of wipes appropriately. To this end, legislation is not about use of plastic per se but is more focused on how they are disposed. This is where we see strategy gaps beyond the impending more stringent approach to product labelling and directions for proper disposal.

Legislators have used beach litter collection data to designate wipes as a problem. Also, wipes continue to find their way into the sewage systems, meaning consumers (at least a group of them) are not following disposal guidelines correctly. Legislators are also pushed by utilities who point to wipes blocking drains and filters and also contributing to the ever-present menace of ‘fatbergs.’

Consumers for their part have seen wipes as a hygiene solution in a time of crisis but the brands who are buys ‘making hay while the sun shines’ have largely failed to support extended wipes usage with campaigns promoting responsible disposal. These are the same brands who are (for the most part) locked into long term plastic reduction commitments.

Responsible Disposal a Key Objective

In the U.S., regulating the disposal of wipes remains a largely state-led effort, with proper labelling practices at the center of the debate. Wipes claiming to be flushable are under increasing pressure to inform and educate consumers with correct and prominent labelling. Washington state set a yardstick for measuring clear labelling by being the first state to legally mandate “do not flush” claim for non-flushable disposable wipes.

Though the prospect of reaching a nationwide sweeping rule remains unclear, ongoing progress does not go unnoticed. In December, Responsible Flushing Alliance, a coalition of trade associations, wipes manufacturers and non-profits, was formed to raise consumer awareness about the proper disposal of non-flushable products, and to start, it has partnered with the California Association of Sanitation Agencies to develop an education campaign in California.

Something’s Got to Give

In conclusion, Euromonitor continues to see a long-term future for home care wipes, as the pandemic has helped to reinforce this in the mind of the consumer. There is also evidence that there is further growth outside of the core North America and European regions. That said, while wipes fundamentally offer convenience, they are also increasingly operating in a very complex environment and are being pulled by often opposing forces which is producing strategy gaps that need to be addressed. The spectre of further regulation while being ever-present is nothing new, but can we really say the same about the operating environment that will exist beyond the pandemic?