09.12.16

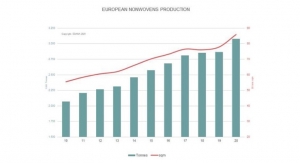

Wetlaid nonwovens, although the smallest nonwovens process type, still maintain an important market share with growth in some markets, notably wipes. They are in an ideal position to address the globally growing demand for more sustainable products. Smithers Pira’s new report, The Future of Wetlaid Nonwovens to 2021 forecasts a market value of $982.6 million by 2021, with a projected annual growth of 5.9%.

Wetlaid nonwovens' ability to use large percentages of low cost, sustainable wood pulp as a raw material makes it one of only a few nonwoven processes that can produce affordable, biodegradable products. Disposability via biodegradation, compostability or even flushability are all possible and somewhat natural extensions of the wetlaid process.

“The wetlaid process is the most versatile in its ability to process diverse fibre types, from fiber glass and carbon to cotton and abaca. This versatility offers both cost and performance opportunities,” says Philip Mango, author of the report.

Wetlaid nonwovens cover many and diverse end uses, including work and hazardous environment garments, interlinings, shoe inserts and synthetic leather goods, coating substrates and household applications. These discoveries allowed wetlaid to enter some of its largest end use markets, like wallcoverings and liquid filtration. Additionally, the use of short cut glass fibers, carbon fibers and other speciality fibres has allowed wetlaid products to enter newer speciality markets such as battery separators and electronic applications.

Wetlaid nonwovens are now slightly weighted toward durable end uses, with about 55%–62% of wetlaid volume and value being consumed by durable end uses. Disposable end uses accounted for 44.9% of wetlaid tons in 2016.

Wetlaid nonwovens are gaining in sustainable market segments, where wetlaid nonwovens’ reliance on sustainable raw materials like wood pulp is a major positive. The inclusion of more wetlaid fiberglass nonwovens as nonwovens by definition has increased estimated and projected consumption. The net result is that wetlaid nonwovens continue to grow and it appears that this modest growth will continue.

The Future of Wetlaid Nonwovens to 2021 is based on an combination of in-depth primary and secondary research. Primary research included interviews with key participants in marketing, sales, production and product development for the entire wovens and nonwovens supply chain. Key participants interviewed included personnel from producers and raw material suppliers, as well as industry experts from major process equipment suppliers and industry consultants. Secondary research included information acquired from technical literature, reports, papers, conference proceedings, company information, and other trade, business or government sources.

Wetlaid nonwovens' ability to use large percentages of low cost, sustainable wood pulp as a raw material makes it one of only a few nonwoven processes that can produce affordable, biodegradable products. Disposability via biodegradation, compostability or even flushability are all possible and somewhat natural extensions of the wetlaid process.

“The wetlaid process is the most versatile in its ability to process diverse fibre types, from fiber glass and carbon to cotton and abaca. This versatility offers both cost and performance opportunities,” says Philip Mango, author of the report.

Wetlaid nonwovens cover many and diverse end uses, including work and hazardous environment garments, interlinings, shoe inserts and synthetic leather goods, coating substrates and household applications. These discoveries allowed wetlaid to enter some of its largest end use markets, like wallcoverings and liquid filtration. Additionally, the use of short cut glass fibers, carbon fibers and other speciality fibres has allowed wetlaid products to enter newer speciality markets such as battery separators and electronic applications.

Wetlaid nonwovens are now slightly weighted toward durable end uses, with about 55%–62% of wetlaid volume and value being consumed by durable end uses. Disposable end uses accounted for 44.9% of wetlaid tons in 2016.

Wetlaid nonwovens are gaining in sustainable market segments, where wetlaid nonwovens’ reliance on sustainable raw materials like wood pulp is a major positive. The inclusion of more wetlaid fiberglass nonwovens as nonwovens by definition has increased estimated and projected consumption. The net result is that wetlaid nonwovens continue to grow and it appears that this modest growth will continue.

The Future of Wetlaid Nonwovens to 2021 is based on an combination of in-depth primary and secondary research. Primary research included interviews with key participants in marketing, sales, production and product development for the entire wovens and nonwovens supply chain. Key participants interviewed included personnel from producers and raw material suppliers, as well as industry experts from major process equipment suppliers and industry consultants. Secondary research included information acquired from technical literature, reports, papers, conference proceedings, company information, and other trade, business or government sources.